5 budgeting methods for better money management

Mike Cramer

Senior Wealth Planning Strategist

While there are a variety of budgeting methods to choose from, many fail because they leave people feeling overwhelmed or restricted. Percentage-based budgeting offers a simpler, more flexible approach by helping you manage your money without tracking every dollar.

Here's how percentage-based budgeting works—and how it can help you simplify your finances, stay on track and build better money habits over time.

Key takeaways

- Percentage-based budgeting simplifies your finances by dividing your income into three categories, offering a practical alternative to more detailed or restrictive methods.

- Popular formulas like the 50/30/20 rule and 80/20 method help you prioritize spending, saving and paying off debt based on your goals.

- Start with a budgeting formula that fits your current situation, and adjust it as your needs change.

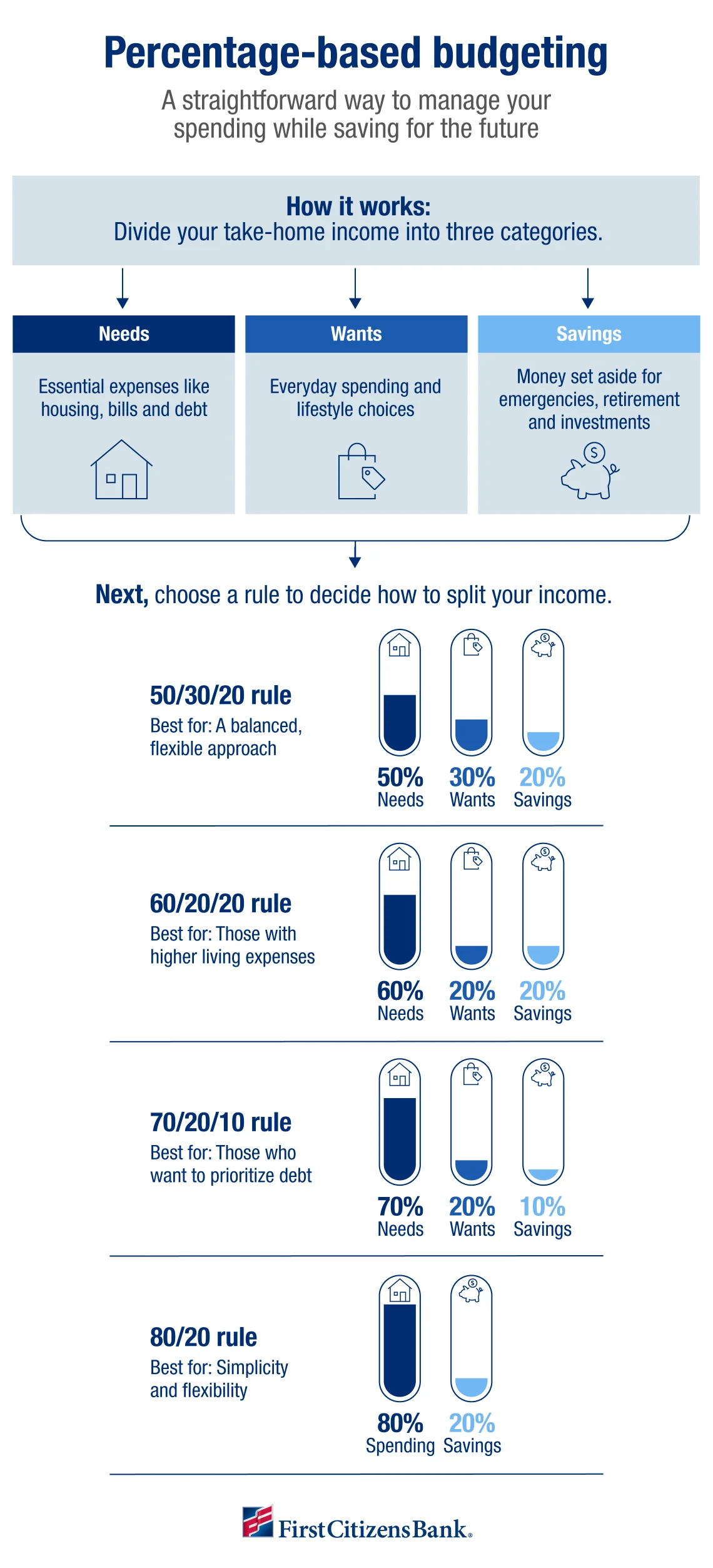

What is percentage-based budgeting?

Also called rules-based budgeting, percentage-based budgeting is a straightforward way to allocate your after-tax income. Instead of relying on detailed tracking or monitoring every transaction, this method uses a set of clear budget guidelines to organize your spending.

Percentage-based budgeting works by dividing your paycheck into three broad categories: needs, wants and savings.

Needs

Needs are essential expenses you must pay to maintain your basic standard of living. They include rent or mortgage, utilities, groceries, transportation, insurance and minimum payments on debts like credit cards, student loans and car loans.

These expenses can be:

- Fixed, meaning they stay the same each month, like a mortgage or car payment

- Variable, meaning they fluctuate, like utilities or groceries

This is the largest portion of a budget for most people.

Wants

This is your discretionary spending. It typically includes expenses like dining out, entertainment, travel and shopping—but it can also cover more purposeful spending, such as a paying for a professional certification or preparing for a new baby.

What falls into this category depends on your lifestyle and priorities. If you're focused on aggressive savings goals, this category may be smaller. If you're aiming for balance—or are in a season of higher spending—it may be similar to, or even larger than, your savings allocation.

Savings

Savings represents money set aside for your financial future. For many people, this is the second-largest category. You can use it to build financial security, save for retirement, prepare for unexpected expenses or save for a specific goal like buying a home or paying for a wedding.

The benefits of percentage-based budgeting

Percentage-based budgeting is popular because it's flexible and easy to follow. It gives you the ability to prioritize what matters most—whether it's paying down debt, controlling your spending, saving for the future or maintaining room in your budget for the things you enjoy.

One of its biggest advantages is adaptability. Because it's built around broad categories rather than rigid line items, you can adjust your allocations as your personal financial plan evolves.

For example, if you want to accelerate student loan repayment, you might temporarily shift more of your income toward debt within your existing categories. Or if you're planning a large purchase—like new furniture—you could redirect funds from your discretionary spending category for a few months until you're ready to buy.

Popular budgeting methods

There are several percentage-based budgeting formulas to choose from—each focused on a different financial priority.

50/30/20 method

The 50/30/20 rule offers a balanced approach, making it a popular method for those new to budgeting. It's designed to help you build savings steadily while still allowing room for discretionary spending.

With this method, 50% of your income goes toward needs, while 30% goes toward wants and 20% goes toward savings.

60/20/20 method

A 60/20/20 budget can be a good option for those looking to balance higher living expenses. With this method, 60% of your income is allocated toward needs, while 20% goes toward wants and 20% goes toward savings—helping to maintain a strong savings rate while accommodating higher fixed costs.

70/20/10 method

This budgeting method is often used by those focused on managing debt alongside everyday expenses. It can provide more room to pay off debt and stay on top of financial obligations while still setting aside money for the future. In this framework, 70% of your income goes toward needs, while 20% goes toward wants and 10% goes toward savings.

80/20 budget rule

Also known as the pay-yourself-first method, the 80/20 rule prioritizes simplicity. You set aside 20% of your income for savings, and the remaining 80% covers everything else—needs, wants and debt. This approach reduces the need for detailed tracking, although it may be less effective if you need tighter control over spending or debt repayment.

60/30/10 +15 method

While less popular, the 60/30/10 +15 method can be a great tool for those looking to catch up on retirement savings.

First, 15% of your pretax income is directed toward a retirement account, such as a 401(k). Then, your remaining take-home pay is divided as follows: 60% goes toward needs and debt, 30% goes toward wants and 10% goes toward additional savings.

This budgeting method can help you maximize employer contributions and reduce taxable income while still maintaining a balanced budget.

How to calculate your budget

Determining how to budget money using these methods will require some calculations. Begin with your monthly take-home income, then apply your chosen percentages to set clear spending boundaries.

For example, someone whose monthly take-home pay is $6,000 and follows a 50/30/20 budget would allocate their paycheck as follows:

Needs (50%): $3,000 for essentials like housing, utilities, groceries and debt repayment

Wants (30%): $1,800 for discretionary spending like dining out, travel and hobbies

Savings (20%): $1,200 toward a retirement account or high-yield savings vehicle, such as a certificate of deposit or money market account

Once you've set these boundaries, the key is consistency. Track your spending throughout the month to make sure you're staying within each category. Over time, the process becomes more intuitive—and easier to maintain.

Choosing the right budgeting method

As you determine which of these budgeting methods is right for you, you'll need to think carefully about your current financial situation by making the following considerations.

Calculate your total monthly expenses

Begin by calculating your essential monthly costs. Add up fixed expenses like rent or mortgage, utilities, insurance and car payments. Then estimate variable essentials like groceries and include the minimum payments on any debt.

If these core expenses take up a large share of your income, a method that allocates more toward needs—such as a 60/20/20 budget—may be a better fit.

Prioritize saving or paying off debt

Your financial goals should shape your approach. For many people, deciding whether to save or pay off debt is an important step. While paying down debt matters, having savings in place can help you handle unexpected expenses without taking on more debt.

- If you don't have an emergency fund: Focus on building one first. Most experts recommend saving 3 to 6 months of essential expenses to help cover unexpected costs like a job loss or medical bills.

- If you have high-interest debt: Consider a method that allows you to direct more toward repayment, such as the 70/20/10 or 80/20 approach. Both options still allow you to set aside money for savings while prioritizing debt payoff.

Not sure where to start?

If you're new to budgeting, a simpler method can make it easier to build consistency. The pay-yourself-first approach prioritizes saving by setting aside 20% of your income up front while giving you flexibility with the remaining 80%.

If you're looking for a more balanced framework—or have struggled to stick with a budget in the past—a 50/30/20 budget is a popular option that works well for many people.

How to customize budgeting rules

Percentage-based budgets are meant to be a starting point, not a rigid formula. You can adjust the budget percentages to reflect your current situation, goals and priorities.

For example, if you're living with family while saving for a down payment and have little or no debt, your essential expenses may be relatively low. In this case, you might shift more of your income toward savings. Instead of following a traditional 60/20/20 split, you could flip it—allocating 20% to needs, 20% to discretionary spending and 60% to savings for your down payment.

The key is to align your budget with your reality. As your circumstances change—whether it's taking on higher housing costs, paying off debt or reaching a major savings goal—you can adjust your budget percentages to match.

The bottom line

Percentage-based budgeting offers a flexible way to manage your money without overcomplicating the process. By setting clear boundaries for spending, saving and essentials, you can stay in control of your personal finances while still adapting to changes in your life.

The key is consistency, not perfection. Start with a framework that fits your current situation, then adjust as your goals and priorities evolve.

Open a 5-month CD

Earn up to 4.00% annual percentage yield.DD

Open an 11-month CD

Earn up to 3.75% annual percentage yield.DD