8 steps to financially prepare for a baby

As a new parent, you want to provide the best for your children. To do so involves planning for some significant changes in your financial life, even before your baby arrives.

To help prepare your finances—whether you're currently expecting, in the process of adopting or just planning ahead—here are eight practical steps to take before expanding your family.

Key takeaways

- As you plan for the arrival of your baby, you can take several steps to help manage expenses, avoid debt and keep your financial life in order.

- Increase savings, review health insurance benefits and plan for childcare well in advance of your baby's arrival.

- As you prepare for this next stage of life, devote time to your long-term finances by revisiting your life insurance coverage and retirement savings plans.

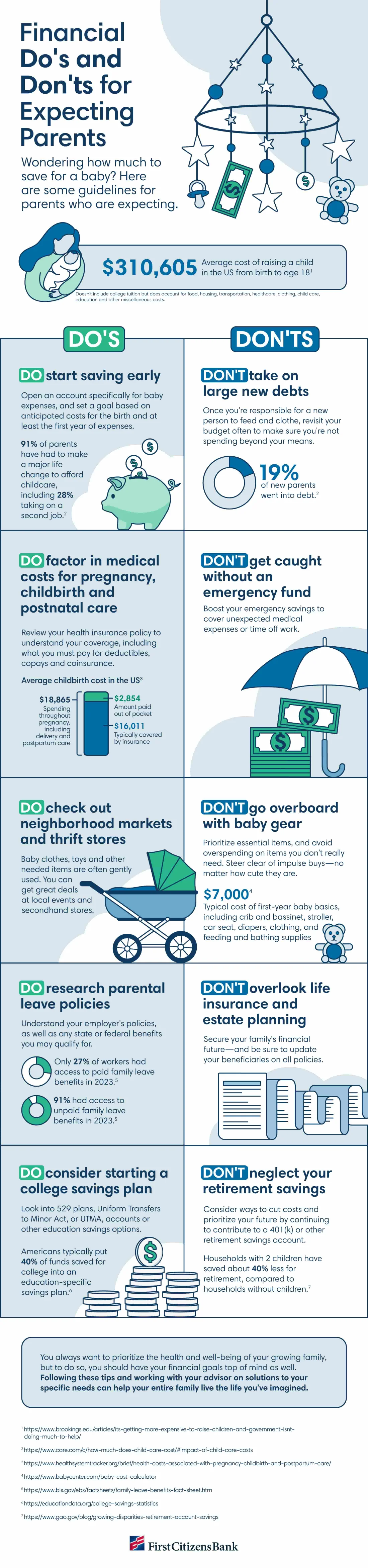

1Start saving now

No matter where you are in your journey, it's time to start saving. Having a healthy savings account balance will put you in a better position to manage unexpected expenses and avoid taking on debt. Here's how to financially prepare for a baby.

- Build up your emergency fund. Ideally, you should stash away at least 6 months of post-baby necessary living expenses to cover unexpected situations like a job loss or major home repair.

- Establish a baby fund. Open a dedicated savings account for baby-related expenses.

- Contribute to your savings consistently. Determine how much you can save per paycheck, and set up direct deposits or automatic transfers from your checking account.

- Put your cash where it can grow. Consider moving some of your baby fund to a high-interest-rate money market account. These accounts can offer higher rates than traditional savings accounts while allowing easy access to funds when needed.

How much should you save before having a baby?

To accurately determine how much money to save before your baby arrives, start with a budget calculator. Every family's financial situation is unique, so tailoring your savings plan to your lifestyle, household expenses and healthcare costs is essential. The good news is you don't have to buy everything at once. For instance, your baby won't immediately need a high chair.

What if you need fertility treatments?

If you're exploring fertility treatments, you're not alone. An estimated 42% of US adults have either undergone fertility treatments or know someone who has, according to Pew Research Center. While the cost of fertility care can be a significant barrier for many aspiring parents, there are several funding options available. Some of the more common ways to pay for fertility treatments include grants, retirement savings, insurance coverage and workplace benefits.

How can you save for adoption?

Although adoption costs can be significant, there are various strategies to help manage and minimize these expenses. Depending on your circumstances, you may also be eligible to use government assistance, adoption grants or tax credits to help fund an adoption. For example, under the One Big Beautiful Bill Act, or OBBBA, signed into law in July 2025, the $17,280 adoption tax credit is now refundable up to $5,000. This change allows you to receive the credit as a refund even if you owe less than $5,000 in federal taxes.

2Build a baby budget

Creating a baby budget gives you a spending plan for essential expenses and discretionary purchases, as well as other financial objectives. Without a budget, it can be easy to overspend, take on debt or fall behind on your savings and investing goals.

How much does a baby cost in the first year?

Your baby's first-year expenses will vary based on your location, lifestyle and other factors like the health of the baby and mother. In addition to budgeting for expected costs like diapers, formula, childcare and other essentials, factor in the costs of parental leave, prenatal care, delivery and an increase in your health insurance premium. Reach out to friends and family members who've recently had children so they can shed some light on these additional costs and how they may affect your spending during the first year.

How to save for a baby on the way

If you're already expecting a baby, you should still have plenty of time to get your finances in order. Start by calculating how much to save for a baby. Then compare this amount to your current savings balance and create a plan to make up the difference. The following steps can help you create an attainable plan.

- Track your spending. Look at your credit card and bank statements to see where your money is going now.

- Estimate expenses. Determine roughly how much you'll spend on baby essentials like medical care, childcare, diapers, formula, clothing and other items.

- Create a budget. Add these estimated expenses along with your monthly bills, like housing expenses, car payments and student loans.

- Adjust as needed. If your budget is tight, find areas where you may be able to cut back, such as unused services or subscriptions. Also look for opportunities to negotiate lower rates with your cell phone, internet, cable and insurance providers.

3Reduce your debt

Learning how to budget for a baby also involves managing and reducing debt. Paying off debt can increase budget wiggle room and reduce anxiety, both of which are essential with a new baby at home.

If possible, aim to reduce or eliminate any credit card balances before your baby arrives. If you're struggling with high interest rates, debt consolidation may be worth exploring. Transferring your balance to a low-interest credit card or taking out a low-interest personal loan may help simplify your bill payments while reducing the amount of interest you accrue each month.

4Review your health insurance policy

Your health insurance coverage may influence how much you'll need to save for a baby. While health insurance can help make pregnancy, delivery and recovery more affordable, you'll likely still be responsible for some out-of-pocket costs. Carefully review your health insurance policy to avoid any unexpected surprises.

If you're uninsured, take steps to secure coverage as soon as possible. If you're ineligible for insurance through a workplace plan, visit HealthCare.gov to explore your options.

Does insurance cover the cost of having a baby?

Health insurance covers some of the cost of having a baby, but coverage amounts can vary. It's a good idea to review your policy to determine how much you may need to pay out of pocket. Be sure to pay close attention to the following items:

- Your deductible: The amount you'll pay before your coverage kicks in

- Your out-of-pocket maximum: The most you'll be required to pay for care

- Copays: A set fee you pay for specific visits and treatments, such as doctor's appointments, specialist appointments, prescriptions and emergency room visits

- Coinsurance: The percentage of the total cost you're responsible for after meeting your deductible

Also be sure to check on additional costs you may be responsible for if you have pregnancy or delivery complications so you're prepared for unforeseen scenarios.

Is pregnancy considered a preexisting condition?

Health insurance companies don't consider pregnancy to be a preexisting condition. This means they can't deny coverage to you or charge a higher premium. But many short-term disability policies consider pregnancy to be a preexisting condition, so you should secure coverage before trying to conceive if your company doesn't provide short-term disability coverage.

How does insurance work once you have a baby?

Once your baby arrives, you'll need to add them to your health insurance policy. Most employer plans allow parents up to 30 days to add a new child to their policy, while health insurance marketplace plans typically allow up to 60 days. Once enrolled, your child's coverage will be effective starting on the date of their birth or adoption. Your insurance premium might increase, so be prepared for a larger bill.

5Plan for parental leave

You'll probably want to take some time off from work to bond with your baby, but doing so can be expensive. The first step to prepare for parental leave is to ask your HR representative about your company's parental leave policy. You should also inquire about any short-term disability benefits your company offers.

Finally, be sure to check your state's family leave laws. Thirteen states currently provide paid family and medical leave, although the specifics vary by state. Additional states are considering similar laws. The federal government also mandates unpaid family leave for employers with 50 or more employees.

6Plan for childcare

The cost of childcare is a key concern for many new parents. Here's how you can develop a solid childcare strategy before your little one arrives.

- Explore your options. Start researching what's available to get a better sense of how much you'll need to pay for childcare. Common options include day-care programs, in-home day care, nannies, and friends and family. Update your post-baby budget to reflect these anticipated expenses.

- Meet with human resources. Some employers also offer dependent care flexible savings accounts, or DCFSAs, to help parents save on child-care expenses. This can significantly lessen the financial burden for new parents. The amount you can contribute to a DCFSA depends on your tax filing status and, in some cases, your income. For the 2025 plan year, the maximum amount is $5,000 for single individuals and married couples filing jointly and $2,500 for married couples filing separately. Also be sure to ask about other potential parental benefits such as on-site childcare, subsidized care or employer contributions to your DCFSA.

- See if you're eligible for assistance. If you think you'll need financial help, visit ChildCare.gov to view a list of government programs that may help with the cost of care.

- Explore tax deductions. The Child and Dependent Care Credit, also known as the Daycare Credit, is designed to offset the cost of childcare while you work or look for a job. Depending on your modified adjusted gross income, you may be eligible to claim up to $3,000 in expenses for one dependent or $6,000 for two or more dependents. In addition, under OBBBA, the Child Tax Credit has increased to $2,200 for each child with a Social Security number. Given the potential benefits, it's wise to research any other tax credits and deductions that may be available to you as a parent.

- Contribute to your child's savings account. Another OBBBA feature is the introduction of savings accounts for children. Through this program, the federal government provides $1,000 in initial savings contributions to US citizens born between January 1, 2025, and December 31, 2028. You can make up to $5,000 non-tax-deductible contributions per year to your child's account. The savings growth is tax-deferred, and withdrawals can begin when your child turns 18.

7Get your affairs in order

Having adequate life insurance and an updated estate plan can help protect your baby if something happens to you. Here are some steps to take to ensure your loved ones are covered.

- Secure life insurance. If you already have a policy in place, you may still need to adjust your life insurance coverage to protect your growing family. You may also want to consider disability insurance to protect your household's income if you become unable to work.

- Review your beneficiaries. Make sure to update the beneficiaries on all financial accounts, including your life insurance policy, retirement savings plan and bank accounts.

- Create or update your will. Work with a lawyer to draft a document that establishes guardianship for your child and spells out who should inherit your property.

During this time, consider establishing a 529 college savings plan for your baby. These plans allow you to save money for your child's education that grows federally tax-deferred and not subject to federal income tax when used for qualified education expenses. The plans are quite flexible and can be used for K-12 tuition and a range of college-level expenses. You can also rollover excess funds from the plan into a Roth IRA for retirement, subject to some restrictions. Once you've established a 529 plan, encourage relatives to make gift contributions instead of toys and gifts.

8Keep saving for retirement

Having a baby will have a significant impact on your finances. As a result, it may be tempting to reduce—or even pause—retirement contributions during this time. However, continuing to contribute to your retirement fund is essential for maintaining long-term financial security. While new expenses may arise, keeping your retirement savings on track can help ensure you're prepared for future needs and can provide a stable financial foundation for both you and your child.

The bottom line

As you prepare for the arrival of your child, many aspects of your life inevitably take a back seat. Take time to speak to a financial advisor to help you plan for this next stage.