Balance transfers

0% introductory APRD for the first 12 monthsD on balance transfers, then variable purchase rate of 13.49% to 22.49% based on creditworthiness applies

Our low-interest Smart Option credit card puts you in charge. Consolidate your credit with lower interest, no annual fee and added protection wherever you make purchases.

Forget the fees

Pay no annual fee and get our lowest interest rate.

Enjoy benefits

Convenient credit card benefits help protect you and your purchases.

Balance transfer

Use our introductory offer on balance transfers to consolidate your debt.

Manage your spending or consolidate higher interest rate balances on our lowest-APR, no-fee credit card.

0% introductory APRD for the first 12 monthsD on balance transfers, then variable purchase rate of 13.49% to 22.49% based on creditworthiness applies

Variable 13.49% to 22.49% APR based on creditworthiness

Variable 25.49% to 28.49% APR based on creditworthiness; each transaction is subject to a 5% fee (minimum $10)

$0 with this no-fee credit card

Pay with your phone

Add your cards to your mobile device and pay securely with Digital Wallet.

Get alerts

Track your accounts and transactions with text and email alerts.

Pay your bills

Automate your bill payments with Digital Banking for extra peace of mind.

Whether you should transfer your balance depends on several factors. In some cases, it can save you money. Use our handy balance transfer calculator to see if it's worth it for you.

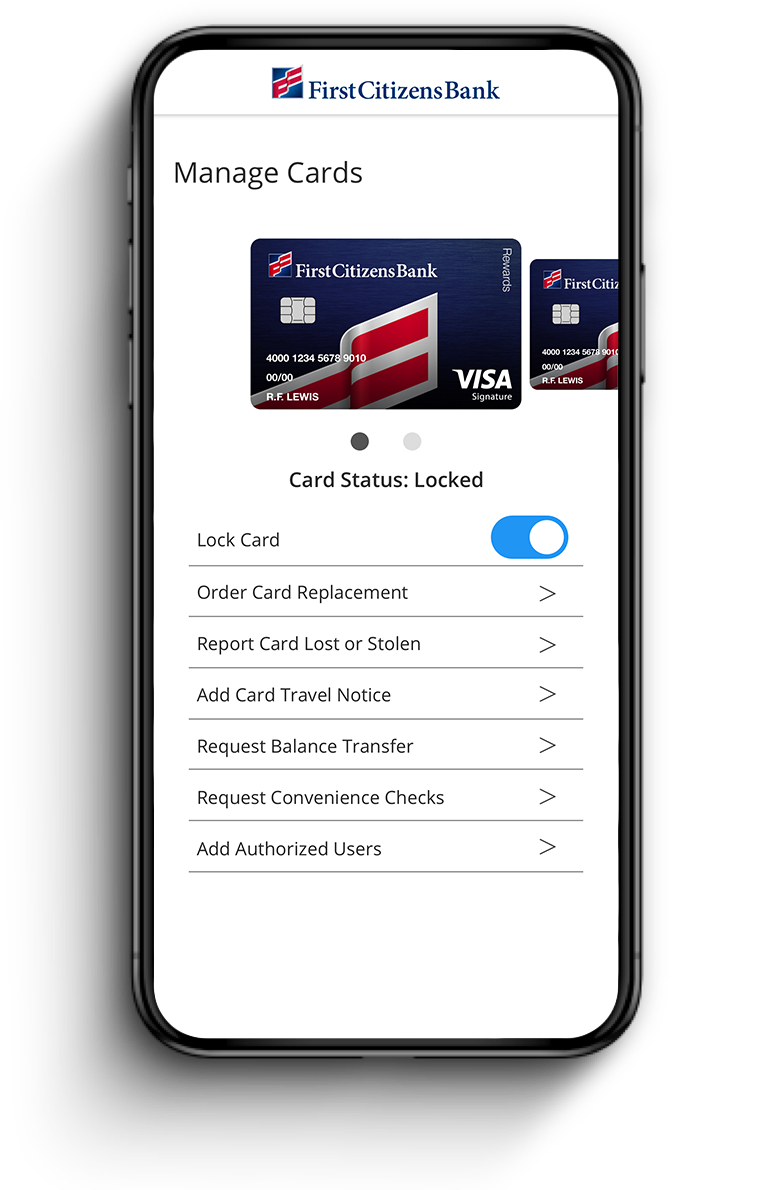

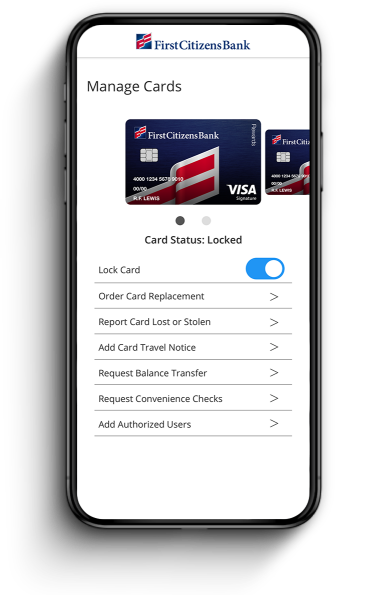

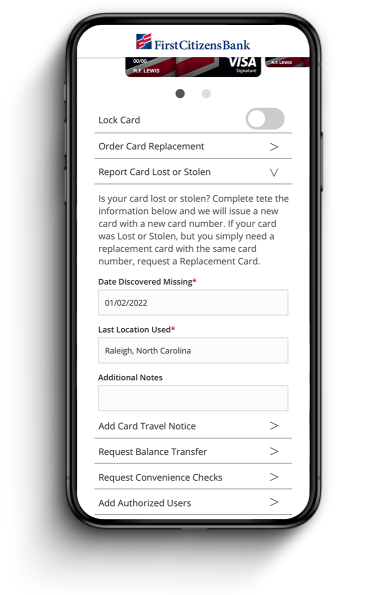

Temporarily lock your card

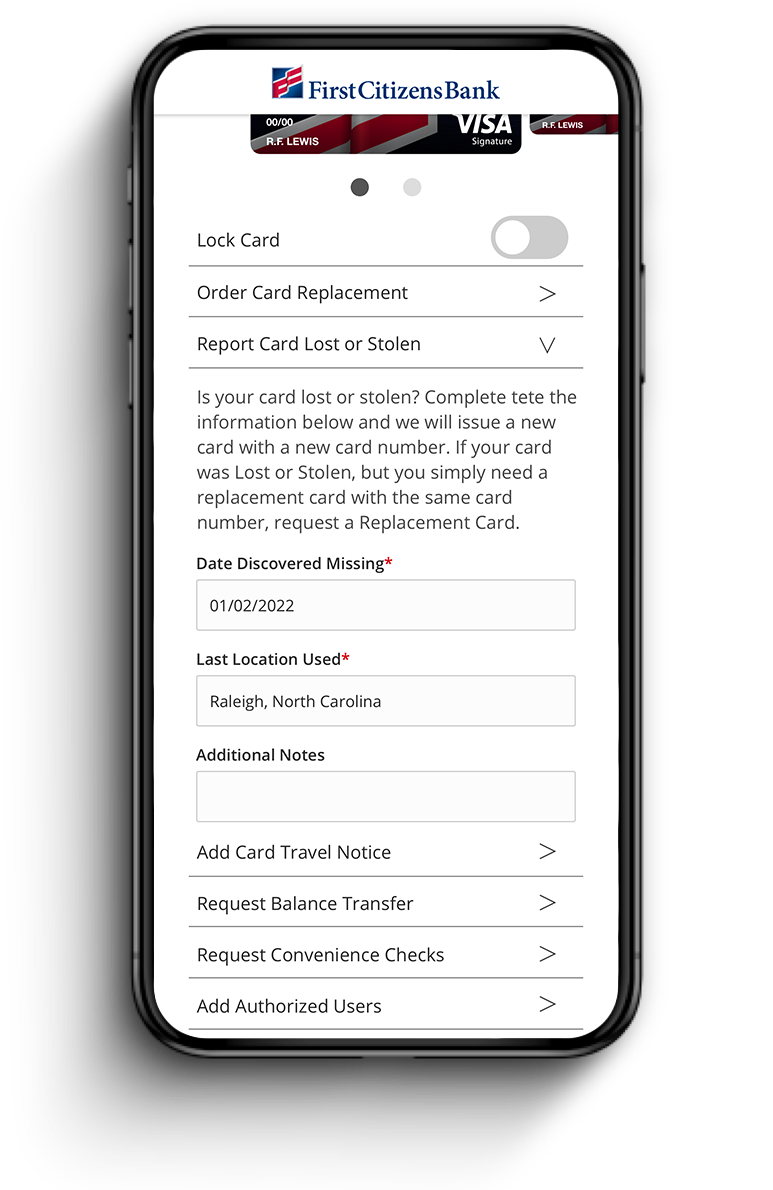

Report a lost or stolen card

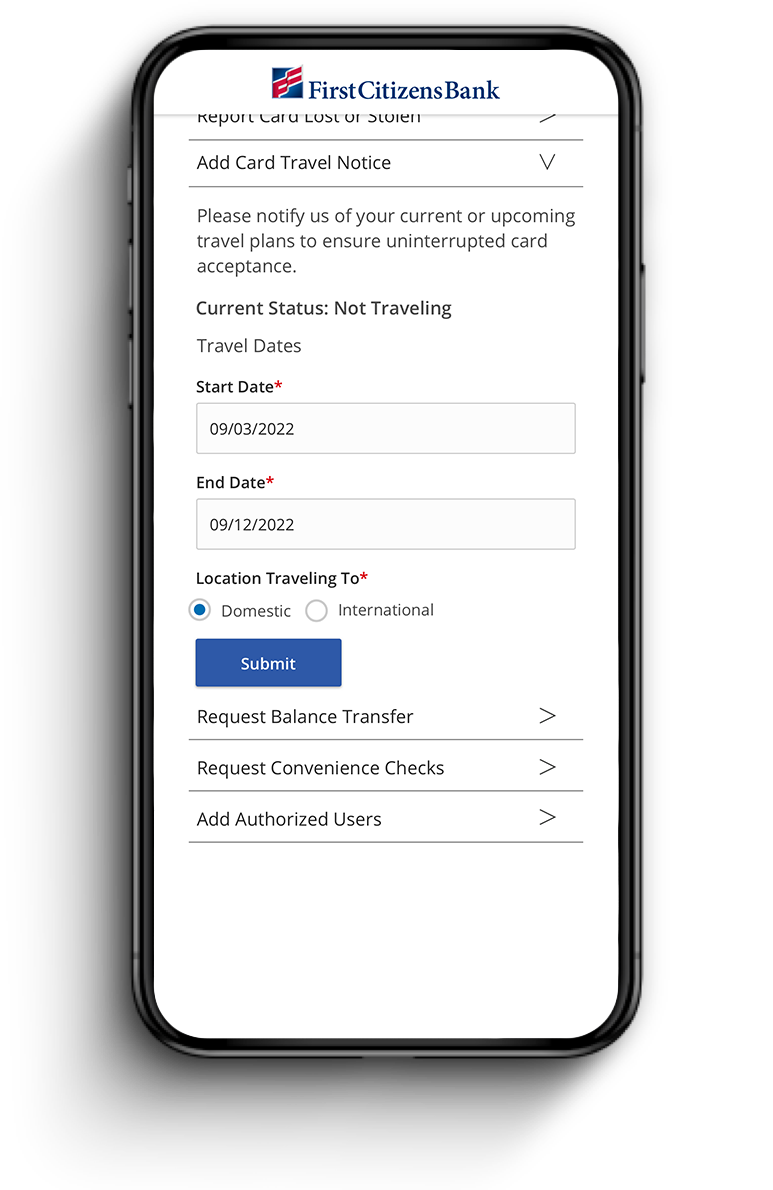

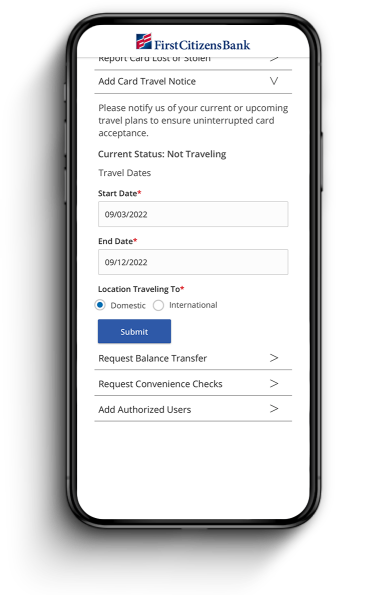

Notify us if you're traveling

Temporarily lock your card

Report a lost or stolen card

Notify us if you're traveling

Treasury & Cash Management

Electronic Bill Presentment & Payment

Investment & Retirement Services

Community Association Banking

Equipment Financing & Leasing

Credit Cards

Merchant Services

Email Us

Please select the option that best matches your needs.

Customers with account-related questions who aren't enrolled in Digital Banking or who would prefer to talk with someone can call us directly.

You are now leaving First Citizens Bank

You are leaving FirstCitizens.com and will be routed to a third-party website that has a different privacy policy than our own. First Citizens Bank and its affiliates are not responsible for the privacy practices, products, services and content on these third-party websites.

You are now leaving First Citizens Bank

You have left FirstCitizens.com. Online brokerage offered by First Citizens Wealth™ is provided through this third-party website which has a different privacy policy than our own. First Citizens Bank and its affiliates are not responsible for the privacy and security practices on third-party websites. To review First Citizens' Privacy and Security practices, visit https://www.firstcitizens.com/privacy-security.

Credit card accounts are available to existing customers enrolled in Digital Banking.

If you don't have an account with us, you can join the First Citizens family with a checking account.

Earn more points on travel and get exclusive travel rewards.

Earn more points on special spending categories.

Transform everyday purchases into unlimited cash back.

Get our lowest available rate.

Still not sure? Compare Accounts

Need to make a change?