What is a trust and how can one help you?

Nerre Shuriah

JD, LLM, CM&AA, CBEC® | Senior Director of Wealth Content and Knowledge

In the world of estate planning, trusts are like Swiss Army knives—powerful and versatile financial planning tools that most wealthy people should become familiar with. Learning about the diverse benefits trusts offer is a great place to begin this process.

Trusts can help you minimize estate taxes and maximize donations in tax-advantaged ways. They can also be used to achieve other goals like funding care for a loved one with a disability or chronic illness or providing for children from a previous marriage. The adaptability of trusts is a key feature, but understanding how they work is essential.

Key takeaways

- A trust is a flexible legal tool that can help manage, protect and transfer assets according to your wishes.

- Different types of trusts—including revocable and irrevocable structures—serve different planning goals, from privacy to tax efficiency.

- Even with higher estate tax exemptions, certain irrevocable trusts can help reduce estate tax exposure and preserve more wealth for beneficiaries.

What is a trust?

Simply put, a trust is a legal arrangement that ensures your assets will be managed according to your wishes during and after your lifetime. To learn more about trusts, however, you'll first need to know about three key stakeholders—the grantor, the beneficiary and the trustee.

- Grantor: The grantor establishes a trust, sets its terms and funds it. A grantor may also be referred to as the settlor, trustor or trustmaker.

- Beneficiary: A beneficiary is anyone entitled to receive the trust's assets. A trust's beneficiaries are selected by the grantor.

- Trustee: The trustee is an individual or institution responsible for managing the trust's assets and carrying out the terms outlined in the trust document.

Two key ways to categorize trusts

It's also helpful to understand two key aspects of trusts—when they're created and whether their terms can be changed.

When the trust is created

- Living trust: Sometimes referred to as an inter vivos trust, a living trust is created and typically funded during your lifetime.

- Testamentary trust: A testamentary trust is established through your will and funded after your death based on its terms.

Whether the trust can be changed

- Revocable trust: The terms of a revocable trust may be revoked or changed while the grantor is alive. Because it must be created during your lifetime, a revocable trust is considered a type of living trust.

- Irrevocable trust: The terms of an irrevocable trust can't be changed by the grantor—although in some states, beneficiaries may petition a court for modifications.

Benefits of trusts

There are many types of trusts, each offering a distinct set of benefits. However, many people choose to establish a trust for the following reasons.

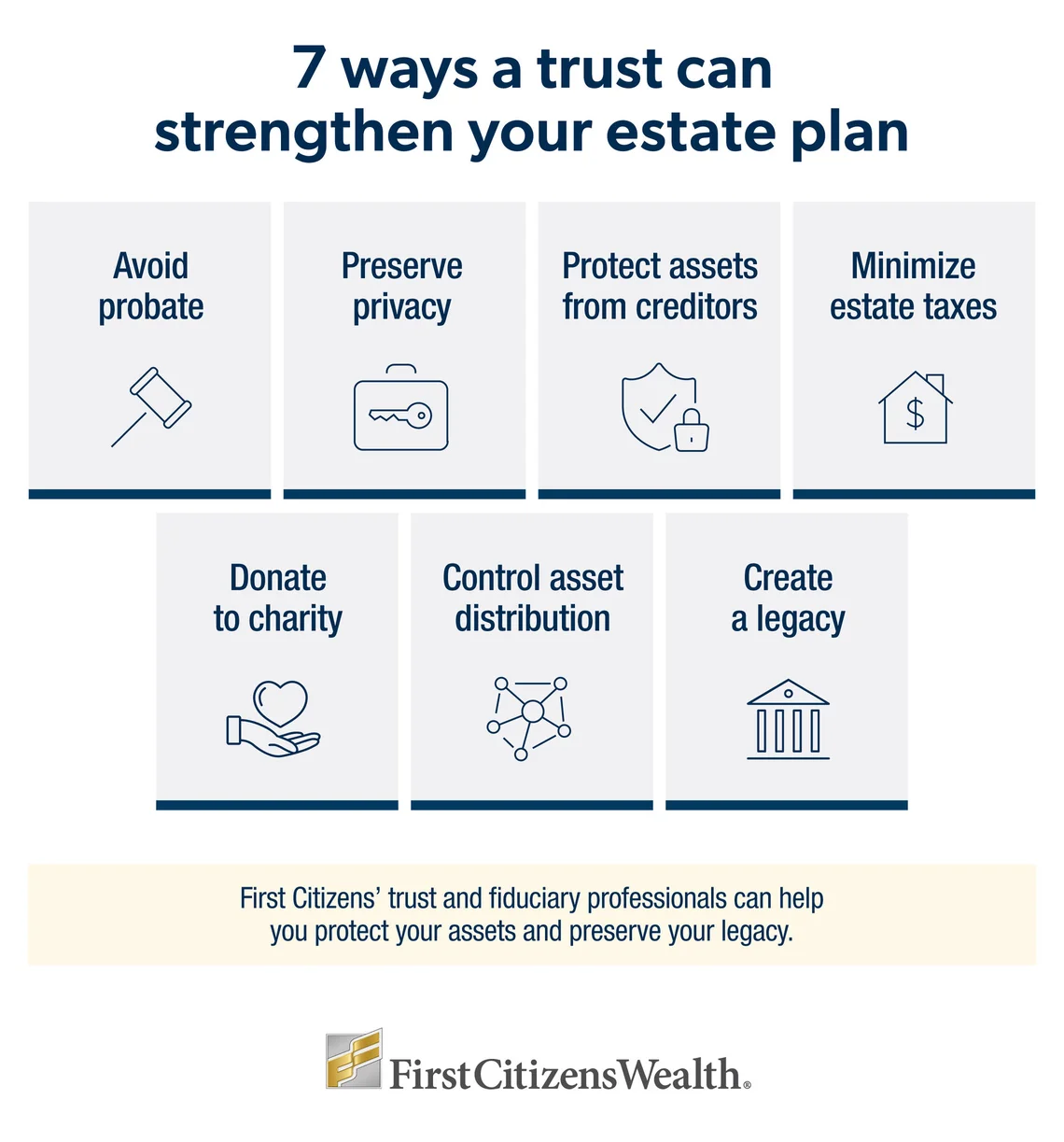

Reducing the risk of probate

If set up correctly, a trust's assets won't be subject to probate, which can be a lengthy and complicated court-supervised process of validating and administering an estate. By avoiding probate, a trust may ease the burden on your heirs to manage your estate after your death.

Increasing privacy

When an estate goes into probate, the details become public record. By comparison, a trust document is typically private, meaning your personal information won't become part of the public record. This distinction can be important to maintain family harmony or prevent fraud.

Shielding assets

Irrevocable trusts can shield assets from creditors and help you minimize estate taxes. However, these benefits are subject to the terms of the trust agreement and applicable federal and state law. Revocable trusts aren't generally created for tax-reduction purposes.

Achieving specific goals

While trusts generally help people transfer and protect assets, there are other reasons you might choose to establish a trust, such as to donate to charity or control how distributions are made to heirs. It's helpful to speak with a financial planner or estate attorney about your reasons for establishing a trust so they can help you determine which type may best meet your needs.

Trusts for minimizing estate taxes

Generally, irrevocable trusts designed to minimize estate taxes are most relevant for individuals and families whose estates exceed—or are projected to exceed—the current federal estate tax exemption. In 2026, the exemption is $15 million for individuals and $30 million for married couples, with automatic annual inflation adjustments going forward.

While the exemption has been permanently increased under recent tax legislation, higher thresholds don't necessarily eliminate estate tax exposure. Sustained market growth, elevated asset values and appreciating assets like closely held businesses or real estate can still push an estate above exemption limits over time.

Irrevocable life insurance trusts

Irrevocable life insurance trusts, or ILITs, are popular among individuals with permanent life insurance policies. Because the ILIT owns and controls the policy or policies, the value of the death benefit is removed from your estate.

Grantor retained annuity trusts

Grantor retained annuity trusts, or GRATs, can be a great tool for individuals and families who expect to see the value of their assets appreciate significantly over time. Using a GRAT may also be worthwhile to split the interest of an asset, allowing you to continue benefitting from it during life and passing the asset at the trust term at a reduced gift tax liability.

Qualified personal residence trusts

Qualified personal residence trusts, or QPRTs, may shield a primary residence or secondary residence from estate taxes. During the term of a QPRT, the grantor can live in the home rent-free. Once the term ends, the grantor would then be required to pay rent. Many people use this technique to pass a vacation home or boat to the next generation.

Spousal lifetime access trusts

Spousal lifetime access trusts, or SLATs, are typically used for lifetime giving between married couples. The grantor spouse transfers assets into the trust, removing those assets from their estate for tax purposes, but the beneficiary spouse and other beneficiaries may receive income and principal during their lifetime. If structured properly, remaining trust assets will pass to designated heirs free of estate taxes.

Trusts for charitable giving

Setting up an irrevocable charitable trust can help you support causes you care about in a tax-smart way. There are two types of charitable trusts available to support charities and your beneficiaries, but they operate inversely to one another.

Charitable lead trusts

By depositing assets into a charitable lead trust, or CLT, the trust will make periodic distributions known as lead payments to your chosen charity. After the lead payments are completed, the remaining assets in the trust are distributed to your selected beneficiaries, effectively reducing both gift and estate taxes.

Charitable remainder trusts

A charitable remainder trust, or CRT, works in the opposite manner. The trust makes income payments to you or your beneficiaries. At the end of the term or upon the death of the last beneficiary, the remaining assets will be donated to your chosen charity. CRTs are a way to obtain income from the disposition of appreciated assets while potentially avoiding capital gains tax liability.

Whether you choose a CLT or a CRT depends on your financial goals and preferences. There are many variations of these trusts, and they're subject to a number of rules and qualification tests. As a result, it's helpful to work with a wealth consultant who can provide valuable guidance.

Trusts for blended families

Estate planning for blended families can be complicated due to the conflicting interests of the parties involved, such as new spouses and children from a prior relationship. There are two types of trust structures that may be beneficial for blended families—qualified terminable interest property trusts, or QTIPs, and AB trust structures.

QTIPS

QTIPs provide shelter from estate taxes while providing income to your surviving spouse. A surviving spouse is the trust's beneficiary during their lifetime—they must receive all income and can access principal if the trust allows. The trust terminates when your surviving spouse dies, and your designated beneficiaries—for example, children from a previous relationship—will receive the assets at that time. This ensures the assets pass to the loved ones of your choosing because your spouse can't select different heirs.

AB trusts

Under an AB trust structure, a grantor establishes two separate trusts that are created upon their death. The grantor's assets are divided between two trusts. Trust A, also called the marital trust, contains assets designated for the benefit of the surviving spouse. Trust B, or the bypass trust, contains assets designated for other beneficiaries, such as children. The provisions included in each trust are selected by the grantor, and some allow surviving spouses to access Trust B if needed—usually after the marital trust is depleted.

Trusts to control distribution

In some situations, your goal may be to exercise guidance over how your heirs spend an inheritance. For example, you might be worried that an heir will make poor spending choices. Alternatively, you may want to ensure your money is spent on educational expenses or provide for a loved one whose disability or chronic illness prevents them from being able to manage their finances. Several trust provisions can be included in the trust document to address these situations.

Spendthrift trusts

A spendthrift provision within a trust allows you to limit the beneficiary's access to the trust income or assets according to terms you define. Depending on your goals, you may also choose to set guidelines on how the money is spent. Spendthrift provisions can also help protect assets from legal claims made by creditors.

Educational trusts

Like the name implies, an educational trust requires a beneficiary to spend the trust proceeds only on educational expenses. Alternatively, the trust can provide for special distributions when the beneficiary makes educational achievements, such as graduating from college, which serves to incentivize desired behaviors.

Special needs trusts

A special needs trust can be used to provide ongoing financial support for an individual with a physical or mental disability or a chronic illness. If drafted correctly, the assets of a special needs trust won't count against the beneficiary's eligibility for needs-based government assistance. Rather, they can supplement expenses not covered by government programs.

Trusts to benefit many generations

When contemplating your estate planning, you may want to set up a plan to have your wealth benefit many successive generations. These trust strategies allow for the preservation of wealth and its continuation.

Dynasty trusts

Sometimes called a legacy trust, a dynasty trust is created in a jurisdiction that has repealed the Rule Against Perpetuities. The state-based rule often requires a trust to terminate after a certain time, such as 90 years after the last beneficiary's passing. Without the rule, trusts based in states that have repealed it can carry on either indefinitely or for a long period of time. The advantage of a dynasty trust is that it's not included in the estate of any generation, yet each generation can benefit from it.

Generation-skipping transfer trusts

A generation-skipping transfer, or GST, trust is an irrevocable trust that designates some assets for heirs two or more generations below the grantor, such as grandchildren or great-grandchildren. Some parents choose to skip their children with a portion of the inheritance, especially if the adult children are already settled in successful careers of their own. The skip keeps the assets from being included in the children's estates and subject to an unnecessary layer of estate taxes. GST taxes offer a shelter amount of $15 million per person, which can be allocated to the skip inheritance.

How to create a trust

The first step when establishing a trust is enlisting the help of an experienced estate attorney. They'll work with you to create a trust document, which will govern the distribution and use of your assets and ensure your trust conforms to federal and state laws.

You can fund a trust with various asset types, such as property, cash and investments. In addition, you can name a trust as the beneficiary of a life insurance policy. In this case, the trust can access the cash value or receive the proceeds from the policy at your passing.

Once funded, the trustee must follow the instructions outlined in the trust document. Trustees have a fiduciary duty to follow the trust's terms and act in the best interests of the trust's beneficiaries—both the income and remainder beneficiaries. Choosing an experienced trustee who understands how to comply with the role's responsibilities is essential, especially for complex trusts.

How trust location can impact outcomes

While a trust's structure is important, where it's established can also influence how it operates over time. Certain states offer legal and tax frameworks designed to support efficient trust administration, enhanced asset protection and long-term wealth preservation. In some cases, working with a trustee in another state may allow you to access these advantages regardless of where you live.

Some strategies that may be supported by favorable jurisdictions include:

- Dynasty trusts: Can be structured in perpetuity to benefit multiple generations without requiring assets to be distributed

- Asset protection trusts: May help shield assets from future creditors, depending on how the trust is structured and applicable state law

- Wealth accumulation trusts: May offer income-tax efficiency, particularly for beneficiaries who reside outside the trust's home state

Delaware is widely recognized as one of the most favorable trust jurisdictions in the US, offering a combination of statutory protections and administrative flexibility that few other states can match. Partnering with an experienced corporate trustee, such as First Citizens Delaware Trust Company, can help ensure your trust is structured and administered in alignment with your long-term goals.

The bottom line

Before you engage an experienced estate attorney to create your trust, you'll need a clear understanding of how a trust can help you achieve your goals. Speaking with a wealth consultant who has detailed insight into your financial situation can help you identify the type of trust that works best for you and your goals.

Your wealth consultant will provide access to a team of specialists—including financial planners, fiduciary officers, estate settlement professionals and insurance specialists. Together, they'll help you make your estate planning goals a reality.