How much is a down payment on a house?

Rob Robertson

SVP, Director of Strategic Sales

Do you really need a 20% down payment to buy a home? Many buyers are surprised to learn that getting a mortgage often requires far less. This guide explains what to know about mortgage down payments and how much you may actually need.

The amount you need for a down payment on a house depends on your loan type, credit score and whether you qualify for a low down payment mortgage program or other assistance. Here, you'll find answers to common questions about how much you need, along with practical tips to help make buying a home more attainable.

Key takeaways

- While a 20% down payment on a house offers many benefits, it doesn't have to be a barrier to homeownership.

- Depending on factors like your credit score, lender and loan type, you may be able to purchase a home with a smaller down payment.

- A mortgage banker or financial advisor can help you determine the down payment amount that makes sense for your situation.

What is a down payment on a house?

A down payment is the portion of the purchase price for a property that you pay for up front instead of financing it with a mortgage loan. Typically, this amount is expressed as a percentage of the purchase price.

A mortgage down payment serves a few purposes. It reduces risk for the lender, which can help borrowers qualify for better terms. It also reduces the size of the loan, which can lower monthly payments. Even though a down payment may seem like a roadblock to homeownership, it can have a positive impact.

What's the average down payment for a house?

Traditionally, the standard down payment for a mortgage has been 20% or more of a home's purchase price. While this benchmark is useful as a reference point, not everyone pays this amount.

For example, the median down payment for first-time homebuyers was 10% in 2025, according to the Profile of Home Buyers and Sellers from the National Association of Realtors. This is because many loan programs and lender options exist that can make it possible to purchase a home with a smaller upfront investment.

What happens if I put less than 20% down on a house?

Many prospective homebuyers wonder whether a lower mortgage down payment will limit their ability to qualify for a mortgage. In many cases, the answer is no. While every lender has their own requirements, homebuyers with excellent credit scores often qualify for a mortgage with a smaller down payment.

Even if your credit score is less than perfect, you may still qualify for a smaller down payment with a government-backed mortgage program. One example is an FHA loan, which is a type of home mortgage that's issued by an approved lender and insured by the Federal Housing Administration, or FHA.

What's the down payment on an FHA loan?

FHA home loans are a popular choice for many buyers with limited savings and less-than-perfect credit. Depending on the lender, borrowers with a credit score of 580 or higher may qualify to make a down payment as low as 3.5% of their home's purchase price. In some cases, borrowers with a credit score as low as 500 may qualify if they make a larger down payment.

It's important to note, however, that all FHA loans require borrowers to carry FHA mortgage insurance. The current upfront premium for this is 1.75% of the base loan amount, which will be due when closing on the mortgage.

Refer to our guide to FHA loans to learn more about the pros, cons and eligibility requirements.

Can I buy a house with no money down?

There are a few mortgage programs that allow qualified buyers to purchase a home without a down payment.

VA loans

Loans backed by the US Department of Veterans Affairs, or VA, allow active service members and veterans to purchase a primary residence with no money down and no mortgage insurance requirement. Typically, VA loans offer competitive interest rates and limited closing costs, potentially saving borrowers thousands of dollars over the life of the loan.

USDA loans

For borrowers in eligible rural areas, USDA loans may be another option. The US Department of Agriculture, or USDA, backs loans that make purchasing a primary residence more affordable for low- to moderate-income borrowers in specified areas. USDA loans don't require a down payment or mortgage insurance, but they do require the payment of an annual guarantee fee, which is typically included in the monthly payment.

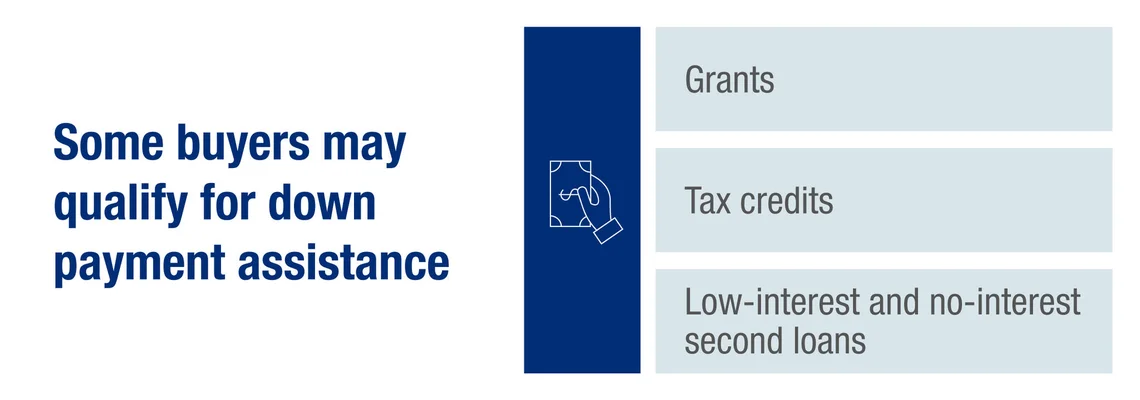

Are there down payment assistance programs?

Many lenders—including First Citizens—offer down payment assistance programs for first-time homebuyers, military service members and public service workers like teachers and healthcare workers. Each lender will have their own rules and eligibility requirements. State, county and city governments may also provide assistance through grants, low-interest second loans or tax credits. A mortgage banker can help you identify programs you may qualify for.

Is it better to put 20% down on a house?

Saving for a down payment of 20% or more may seem burdensome, but doing so comes with two significant financial benefits.

- No mortgage insurance: Loans with less than 20% down typically require private mortgage insurance, or PMI. A 20% down payment means you'll avoid paying this additional monthly fee.

- A lower interest rate: A larger down payment for a mortgage can also help you qualify for a lower interest rate, which can save you tens of thousands of dollars in interest payments over the life of your loan. Use our mortgage comparison calculator to see how much the difference could be.

How do down payments affect mortgage payments?

A larger down payment generally lowers your monthly mortgage payment because you're borrowing less and may qualify for a lower interest rate. While mortgage insurance costs can also decline as your down payment increases, these savings are typically smaller than the reductions in principal and interest.

Here's an illustration of how different down payment amounts may affect monthly payments, assuming a 30-year fixed-rate mortgage at a 6% interest rate. Note that these examples don't account for potential interest rate savings that may result from a larger down payment. PMI estimates are based on Freddie Mac's PMI calculator.

Sample down payments for a $300,000 house

Home price |

Down payment |

Monthly principal and interest |

Monthly mortgage insurance |

Total monthly payment |

|---|---|---|---|---|

$300,000 |

$15,000 (5%) |

$1,708.72 |

$269 |

$1,977.72 |

$300,000 |

$30,000 (10%) |

$1,618.79 |

$173 |

$1,791.79 |

$300,000 |

$45,000 (15%) |

$1,528.85 |

$70 |

$1,598.85 |

$300,000 |

$60,000 (20%) |

$1,438.92 |

$0 |

$1,438.92 |

These examples also exclude homeowners insurance, property taxes and any community association dues. Use our mortgage payment calculator to tailor these estimates to your situation.

Is a down payment the same as closing costs?

When buying a home, you should also be prepared to pay closing costs—sometimes referred to as settlement costs. These upfront fees aren't part of your down payment and may include:

- Loan origination fees

- Government recording costs

- Appraisal fees

- Credit report fees

- Lender origination fees

- Title services fees

- Tax service fees

- Survey fees

- Attorney fees

How much are closing costs?

Closing costs will vary depending on your location and your lender, with the typical tab falling between 3% and 6% of a home's purchase price. For example, you might pay anywhere from $6,000 to $12,000 in closing costs for a $200,000 home.

A portion of these fees is paid to third-party providers, so it's a good idea to shop around for the best deal.

Can I use retirement savings for a down payment?

It's possible to use some or all of the funds from a retirement account for a down payment. However, be aware that different retirement accounts have different rules, timelines and limits.

Traditional IRA

First-time homebuyers can withdraw up to $10,000 from their traditional IRA for a down payment without incurring an early-withdrawal penalty. However, you'll have to pay income taxes on the withdrawal.

Roth IRA

If you've been contributing to a Roth IRA for at least 5 years, you can withdraw those contributions—but not the earnings—penalty- and tax-free.

401(k)

If you withdraw money from a 401(k), you'll have to pay income tax on the withdrawal, and you'll pay a penalty if you're younger than 59 1/2. If you use the money to buy a house, however, some plans may consider this a hardship distribution and waive the early-withdrawal penalty. You should always check with your employer's plan administrator to confirm the rules prior to making any withdrawal.

Some 401(k) plans may allow you to take a loan from your account, which you'll need to pay back with interest. You may have up to 5 years to pay this back—or less, depending on your plan's rules. Note that if you were to leave your job or get laid off, you'd likely have to repay the loan within a specified period.

It's also important to note that withdrawing or borrowing money from your retirement savings will have short- and long-term financial consequences. Consult a financial advisor to determine if this is a good option for you.

What other options do I have?

A piggyback loan could be one strategy to consider. You may be able to avoid paying PMI by working with your lender to source a second loan that will give you enough money for a 20% down payment. Just be sure that the interest you'll pay on this second loan is less than the monthly mortgage insurance amount you'd have to pay with just the first mortgage.

Buyers who already own a home and have sufficient equity may have additional options. One example is a bridge loan, which can provide short-term funds for a down payment when you’re buying a new home before selling your current one. The loan is typically repaid with the proceeds from the sale of the existing home.

A mortgage banker can help you evaluate whether the costs and added complexity of alternative approaches make sense in your situation. For additional insight, refer to our step-by-step guide to buying a home. And once you're ready to explore your borrowing options, learn more about how to shop for a mortgage.

How can I save for a down payment faster?

Creating a plan to save for a down payment on a house can make the goal feel more manageable. Consider these tips.

- Set a clear target so you can create a realistic savings timeline.

- Keep savings in a dedicated account to reduce the temptation to spend.

- Automate deposits to help you build savings consistently over time.

- Ask family members and close friends for contributions to your down payment fund in lieu of gifts.

The bottom line

A 20% down payment on a house isn't mandatory. FHA, VA and USDA loan programs offer options with lower or no down payments, depending on your credit and eligibility. By exploring assistance programs, planning your savings and consulting experts, homeownership can become more achievable.

Explore more down payment options

Homeownership may be closer than you think.