How to reduce taxes in retirement

Retirement should be about pursuing your unique passions, spoiling your grandchildren or buying the vacation home of your dreams—not stressing over how long your savings will last. Knowing how to reduce taxes in retirement is key to preserving as much of your nest egg as possible.

While claiming tax breaks is a helpful starting point, comprehensive tax planning can play a critical role in reducing your overall tax burden in retirement. Here are a dozen strategies that can help serve as conversation starters with a financial or tax professional.

Key takeaways

- Manage taxable income by coordinating Roth conversions, required minimum distributions, or RMDs, and withdrawal strategies.

- Use tax-efficient giving and investing strategies like qualified charitable distributions, or QCDs, donating appreciated assets and favoring lower-tax income sources.

- Make major retirement decisions carefully—including when to claim Social Security and where to live—to help minimize taxes and related costs.

1Take advantage of Roth accounts

Investing in Roth retirement accounts is one proven way to reduce taxes on retirement income. Unlike traditional retirement accounts, contributions made to a Roth 401(k) or Roth IRA are after-tax contributions. However, you'll never pay taxes on this money again. Your savings in these accounts will grow tax-free, and you can make tax-free withdrawals in retirement—as long as you meet certain conditions.

Once you turn 50, you're eligible to make catch-up contributions to further boost your retirement savings. There's even a super catch-up contribution available for people between the ages of 60 and 63 who participate in a workplace retirement plan.

2Minimize RMDs

The IRS mandates annual withdrawals from traditional 401(k) and IRA accounts once you turn 73, or 75 for those born after 1960. These RMD withdrawals are taxed as ordinary income. A large RMD can push you into a higher income tax bracket, increasing the amount of taxes you owe in that year.

However, Roth IRAs and Roth 401(k)s don't require RMDs during the original owner's lifetime. If most of your assets are in traditional accounts, it may make sense to convert some portion of these savings into a Roth 401(k) or Roth IRA before you start taking RMDs. You'll have to pay taxes on the funds in the year you make the conversion, but you'll get all the advantages of a Roth account going forward.

Because of the upfront tax liability, you may want to consider a conversion plan, incorporating options in phases or right after retirement when your income and tax bracket may be lower. Whether this will save you money in the long run depends on many factors, including your tax rate, income level and retirement goals.

3Make QCDs

If you have a traditional IRA but don't need your RMD to fund your living expenses in retirement, you could make a QCD directly from your IRA. You won't be taxed on the distribution, and you'll make progress on your philanthropic giving goals.

Generally, charitable donors who are 70 1/2 or older can transfer a significant amount—$111,000 in 2026—from an IRA directly to qualified charities. Donors who must take RMDs can apply a QCD against the required amount they must withdraw. This option isn't available for 401(k) accounts, so you might consider a rollover IRA if you want to make a QCD.

4Maximize tax deductions

Once you reach age 65, you're eligible for a higher standard deduction. In addition, under the One Big Beautiful Bill Act, or OBBBA, signed into law in 2025, some seniors may qualify for a temporary bonus deduction per eligible filer for tax years 2025 through 2028.

Many tax breaks are available whether you take the standard deduction or itemize, but itemizing may unlock additional savings for some retirees. Commonly overlooked deductions include state sales or income tax, out-of-pocket charitable contributions and certain mortgage refinancing points.

Deducting medical expenses is another frequently missed opportunity. Unreimbursed medical expenses are deductible once they exceed 7.5% of your adjusted gross income, or AGI—a threshold that may be easier to meet in retirement due to higher healthcare expenses and lower income. Also, some states have a lower AGI threshold for medical expense deductions, which may enable you to claim medical deductions at the state level even if you don't qualify federally.

Also make sure you're deducting all medical expenses allowed by the IRS or your state of residence. Health insurance premiums are deductible, and even expenses like acupuncture and health club memberships may be deductible in certain situations.

5Shift to low-tax income investments

When you retire, it often makes sense to focus on tax-efficient investing by allocating part of your portfolio to income-generating investments that aren't taxable or are taxed at lower rates.

For example, interest generated from investments in most municipal bonds is exempt from federal taxes, while interest earned on US Treasury bonds is exempt from state and local taxes. Some real estate investments, such as rental properties, may also have a minimal tax impact because owners can offset rental income with depreciation.

Another lower-tax income investment option is qualified dividend stocks because the income these investments generate is taxed as capital gains rather than ordinary income.

6Make tax-efficient retirement account withdrawals

When you withdraw money in retirement, which account you tap into can greatly impact the amount of taxes you owe. One strategy many retirees use is a proportional withdrawal approach. After determining how much income you need for the year, you would take distributions from each account based on its percentage of your overall retirement savings. This method can help smooth taxable income from year to year and potentially reduce lifetime taxes by spreading the tax impact more evenly over time.

However, no single withdrawal strategy fits every retiree. Your financial plan should take into consideration all potential impacts for your situation and coordinate withdrawal strategies across various retirement income sources—including Social Security and RMDs.

7Manage capital gains thoughtfully in retirement

Capital gains from taxable investments can also affect your tax bill in retirement. In some years, retirees may be able to realize long-term capital gains at a 0% federal tax rate if their taxable income remains below certain thresholds—often early in retirement before RMDs or Social Security benefits begin.

But even when capital gains are taxed at lower rates, they still count toward AGI and may affect the taxation of Social Security benefits or Medicare premiums. As a result, decisions about when to sell appreciated assets—and whether to use strategies such as tax-loss harvesting to offset gains—should be coordinated with other income and withdrawal decisions.

It's also important to consider the impact of the 3.8% net investment income tax, which applies to taxpayers whose modified adjusted gross income, or MAGI, exceeds certain thresholds.

8Tap into your HSA

HSA withdrawals used for qualified medical expenses remain tax-free in retirement. Because healthcare costs tend to rise with age, using HSA dollars to pay for eligible expenses may reduce the amount you need to withdraw from taxable or tax-deferred retirement accounts, which can help keep your taxable income lower.

There's also no deadline to reimburse yourself for qualified medical expenses as long as these expenses were incurred after you established your HSA. Some people choose to pay medical costs out of pocket and allow their HSA balance to continue growing tax-deferred, then reimburse themselves a later year. This approach can provide additional flexibility and preserve tax-advantaged growth for as long as possible.

After age 65, HSAs also become more flexible. You can withdraw funds for nonmedical expenses without paying a penalty. These withdrawals are still taxed as ordinary income, so they don't provide the same tax benefit as using the funds for medical expenses but can serve as an additional source of liquidity if needed.

9Donate appreciated assets to charity

Giving long-term appreciated assets, such as stocks or bonds, directly to charity may help you meet your philanthropic goals—and save on taxes—because donating appreciated assets means you won't need to pay capital gains taxes on the increased value. Plus, you may be able to deduct the fair market value of the assets at the time of donation if you itemize deductions on your tax return.

Keep in mind that certain limits apply, and the amount you can deduct for charitable contributions may vary based on your income level, the type of asset donated and the organization receiving the gift.

10Wait to claim Social Security

While not technically a tax, you'll want to keep the Social Security earnings test penalty in mind if you plan to work while receiving benefits. If you claim benefits before reaching full retirement age and continue to earn income, a portion of your benefits may be temporarily withheld once earnings exceed certain limits.

The good news is the earnings test becomes less restrictive in the year you reach full retirement age and goes away entirely once you reach that age. At that point, your monthly benefit is increased permanently to account for benefits previously withheld.

11Watch out for Medicare premium hikes

Like the Social Security earnings test, higher Medicare premiums aren't technically a tax. However, Part B and Part D premiums are subject to Medicare's income-related monthly adjustment amounts, known as IRMAA, which are based on your income from 2 years prior. Because IRMAA uses a tiered structure, even a small increase in income can result in higher Medicare costs.

While IRMAA shouldn't drive decisions on its own, it's an important factor to weigh as part of broader retirement income planning with a financial advisor.

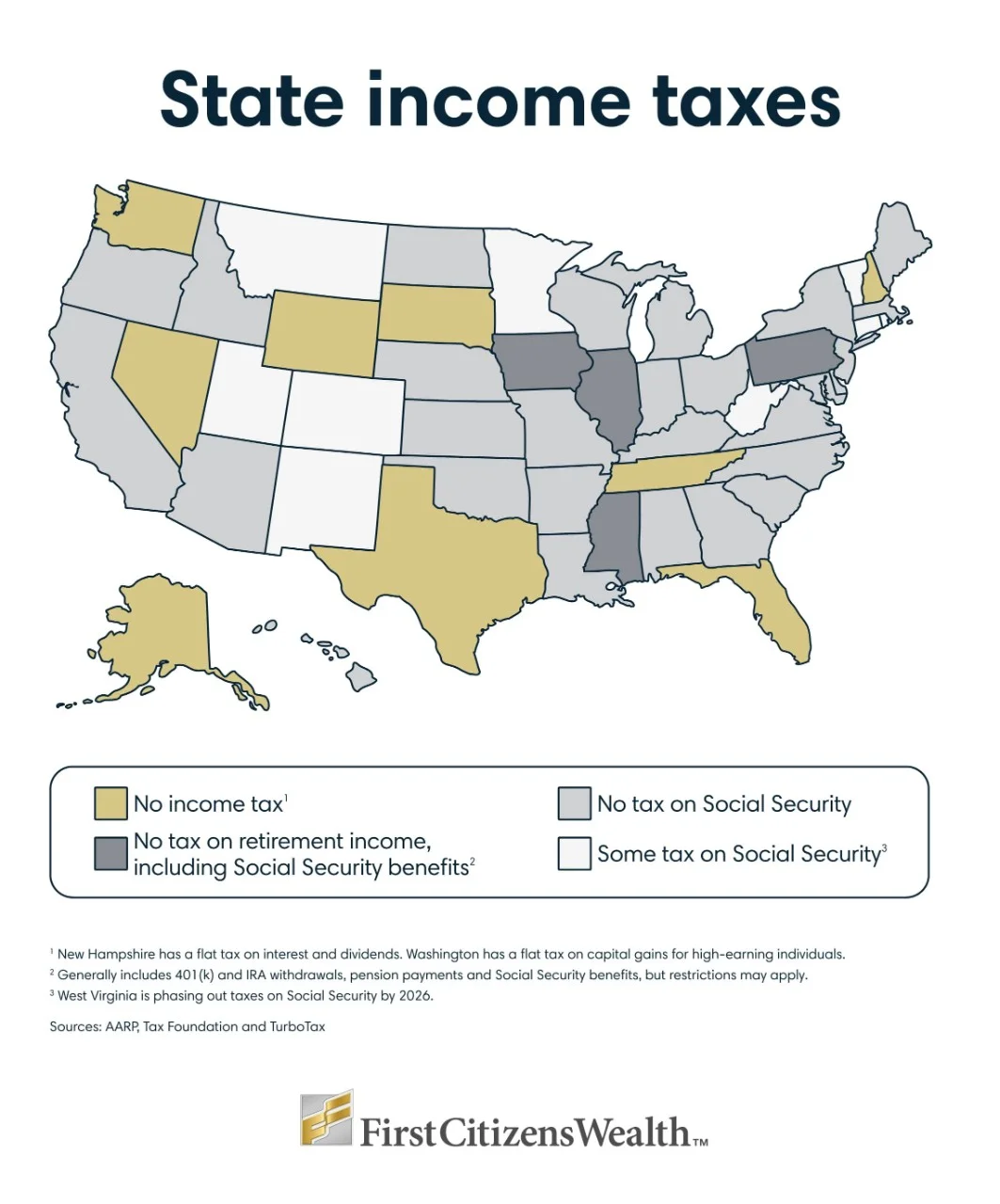

12Consider tax-friendly states for retirees

High state taxes can take a big bite out of your nest egg over time. Fortunately, there are states that don't tax income—and some that don't tax retirement income. If you're thinking about moving to another state in retirement, be sure to factor state tax rates into your decision.

As of 2026, eight states have no income tax at all. However, these states may impose higher property taxes or sales taxes. Notably, Washington imposes a flat income tax, but only on capital gains income for high earners. Another four states tax regular income but not retirement income—401(k) and IRA withdrawals—subject to some restrictions.

Keep in mind that state tax policies can change. For example, at least seven states are actively considering income tax reductions or other reforms, so it's important to review current laws before making relocation decisions.

The bottom line

Deciding how to reduce taxes in retirement will depend on your goals, types of retirement accounts and overall financial picture. Thoughtful retirement income planning is an important part of long-term nest egg preservation, but it can become complex quickly.

This is why enlisting the help of qualified professionals is a smart move. A financial advisor can help you create a holistic retirement income plan—one that meets the needs of your specific situation while keeping an eye on tax efficiency.