Digital banking for business

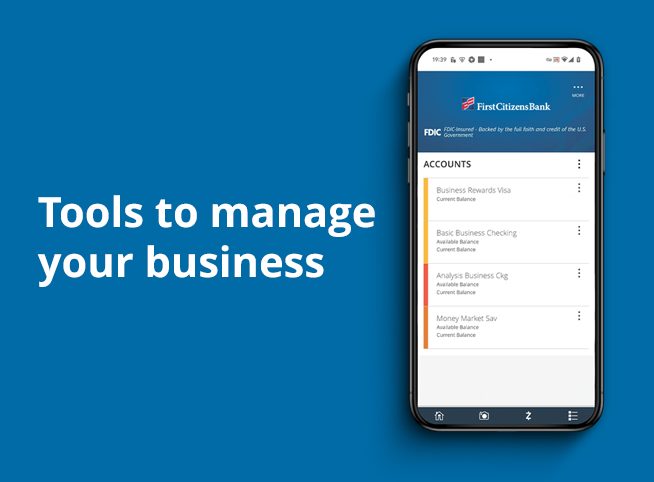

Seamlessly access all of your accounts from one place with First Citizens Digital Banking for business.

Invest how you want, when you want, in real time with Self-Directed Investing.

Seamlessly access all of your accounts from one place with First Citizens Digital Banking for business.

We're committed to serving companies as they expand and succeed. The proof is in our success stories.

2026 Market Outlook video: Available now

The Making Sense team reflects on 2025 and discusses key headwinds and tailwinds for 2026.

Many people are uncertain how to start saving for retirement. If you haven't made saving a major part of your financial life up until now, it's hard to take up a new habit.

Plus, there are so many myths about the best ways to save, and they can make retirement planning more confusing than it needs to be. Here's a look at some of the most common misconceptions—and the truth behind how to start saving for retirement now.

If your employer offers a match on your retirement savings, it's almost always a good idea to opt in. By doing so, you're effectively taking advantage of free money being contributed into your retirement plan while you put away your own money.

But if you don't have this benefit, saving for retirement on your own is still worthwhile. Thanks to the power of compound interest, your money can grow over time. If you invest over several decades, you can end up with a significant nest egg.

To see how powerful compound returns are, take a look at an example using a compound interest calculator. Let's say you start saving for retirement at age 28 and invest $250 per month. If your money earns a return of 6% per year and you keep saving steadily until age 65, you'll have more than $381,000 when you reach retirement age.

In addition to traditional retirement savings, it's also a good idea to consider contributing some of your income to a Roth IRA. A Roth IRA can provide several layers of benefits in saving toward your retirement goals, including potential tax benefits down the line and more flexibility when it comes to withdrawing funds.

People sometimes avoid saving for retirement when they aren't sure how to do it and assume that they can catch up later. Unfortunately, this can be a costly mistake. The longer you wait to start saving, the less you can harness the power of compound returns.

Consider another example. Let's say instead of starting to save at 28, you wait until you're 45 when you have higher earnings. You now start investing $600 per month and continue until age 65. In this case, you'll only have about $264,000 in retirement savings—a shortfall of more than $117,000 compared to what you would have accumulated if you'd started earlier with smaller monthly contributions.

Ultimately, it’s important to start with what you can. The key is to maintain a disciplined approach and remain committed to increasing this amount whenever there are salary increases, holiday or special bonuses, payoffs of other obligations, or debts and household costs that go away. Over time, you can look back and be proud of the sustained activity and accumulation you fed into your retirement.

It's understandable if you feel unsure about how much to save for retirement. It can take some time to learn about retirement planning and determine the best savings rate for your situation. You may find it helpful to use a retirement savings calculator to explore possible scenarios and get a feel for what level of monthly retirement contribution would make sense.

However, even if you're still coming up with a plan, it's important to begin saving to take advantage of compound returns. Starting early so you can save as much as you're currently able to is more ideal than waiting until you've determined the perfect savings rate. You can always change the amount you set aside each month going forward, but you can't go back in time and make up for a year when you didn't save at all.

It's reassuring to know that Social Security benefits can replace some of your income when you retire. But being eligible for Social Security doesn't mean you don't have to save. According to the Social Security Administration, people typically need about 70% of their pre-retirement income to live on in retirement. So if you're making $50,000 per year, you probably need about $35,000 per year when you're retired, or a bit more once you take into account factors like inflation.

Social Security benefits usually replace around 40% of pre-retirement income for the average person. So in general, you can't count on Social Security benefits to completely meet your needs in your golden years.

Building up savings early is ideal, but it's never too late to begin preparing for retirement. If you're close to retirement age, the US Department of Labor recommends cutting your spending so you have more money available to save.

You may also want to look into catch-up contributions, which allow people older than 50 and enrolled in certain eligible retirement plans to contribute more money than the traditional limits. These catch-up contributions for employer-sponsored plans can be up to 33.3% more than the usual limits, allowing you to be more aggressive with your saving strategy.

There's no time like the present to start saving for retirement. Whether you've just embarked on your career or have been in the workforce for years, you might benefit from a tax-advantaged retirement account like a traditional or Roth IRA. Understanding your full options for retirement savings plans will help you decide which path is right for you as you look toward the future.

Treasury & Cash Management

Electronic Bill Presentment & Payment

Investment & Retirement Services

Community Association Banking

Equipment Financing & Leasing

Credit Cards

Merchant Services

Email Us

Please select the option that best matches your needs.

Customers with account-related questions who aren't enrolled in Digital Banking or who would prefer to talk with someone can call us directly.