Roth IRA versus traditional IRA: Eligibility, taxes and rules

Tammy Harrison

VP, Personal Trust IRA Manager

Whether your goal is to grow your retirement savings, reduce your current tax bill or reap tax benefits in retirement, an individual retirement account, or IRA, can play a powerful role in your strategy. However, the benefits you receive depend largely on whether you choose a Roth or traditional IRA.

Understanding the key differences between traditional and Roth IRAs—including eligibility requirements, tax treatment and withdrawal rules—can help you select the option that best aligns with your income, timeline and retirement goals.

Key takeaways

- Both traditional and Roth IRAs provide a tax-advantaged way to save for retirement, but they differ in how and when you receive tax benefits.

- Traditional IRAs offer an upfront tax deduction and tax-deferred growth, while Roth IRAs offer tax-free withdrawals in retirement.

- Other factors—including your annual income, expected future tax rate and long-term retirement strategy—may influence which type of IRA is right for you.

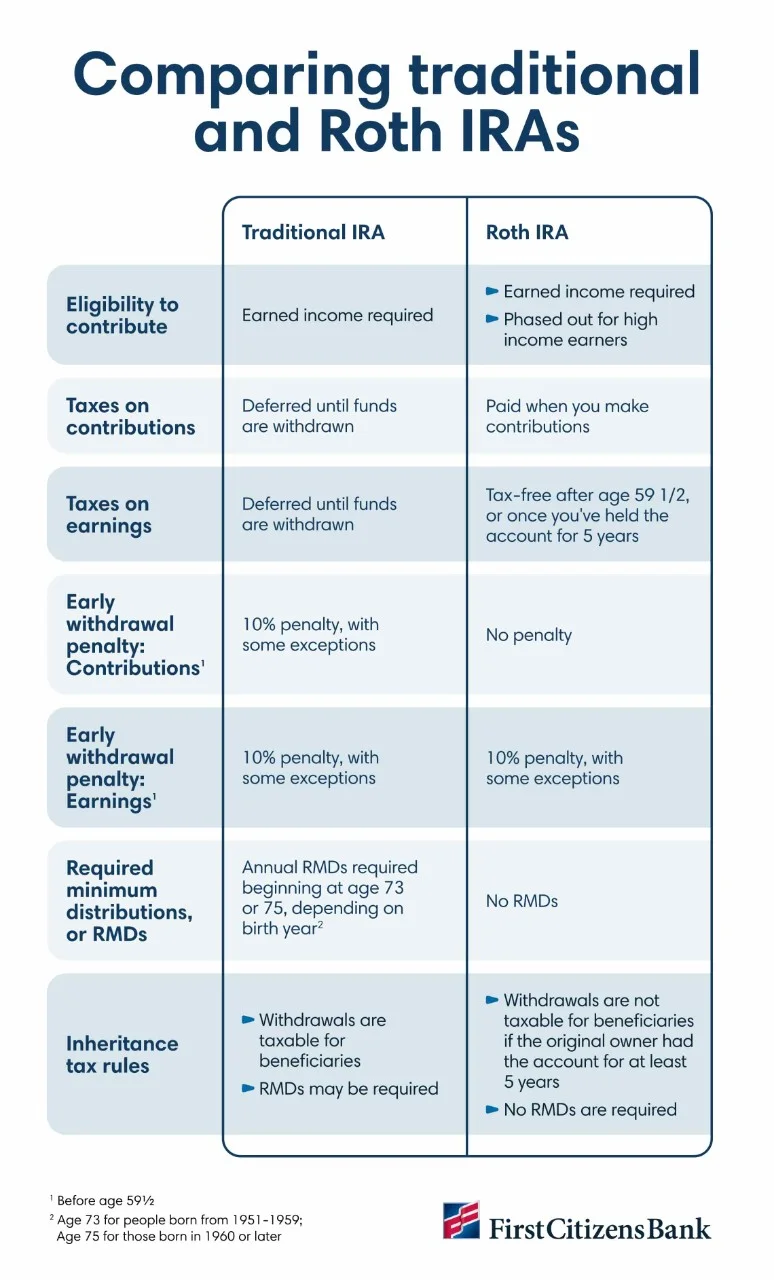

What are the differences between traditional and Roth IRAs?

One of the first steps to opening an IRA is choosing between a Roth IRA and a traditional IRA. While both offer a tax-advantaged way to save for retirement, they differ in income eligibility requirements, withdrawal rules and when you receive tax benefits. Understanding these distinctions can help you select the option that best aligns with your financial goals and long-term retirement strategy.

Overview of traditional IRAs

Traditional IRAs offer current-year tax benefits by allowing you to deduct your contributions each year. Your investments will grow tax-deferred in the account until you're eligible to take qualified distributions, which will then be taxed as regular income.

- Eligibility: Anyone with earned income can contribute to a traditional IRA. However, if you or your spouse has access to a workplace retirement plan, your ability to deduct your contributions may be reduced or phased out based on your income.

- Contribution limits: The IRS sets annual contribution limits for traditional IRAs, and these limits may change from year to year. Higher contribution limits—known as catch-up contributions—are also available for those who are 50 and older.

- Early withdrawals: Early withdrawals before age 59 1/2 may be subject to a 10% penalty in addition to income taxes, although there are some exceptions for penalty-free IRA withdrawals.

- Withdrawals in retirement: Distributions are taxed as ordinary income. You're also required to take required minimum distributions, or RMDs, starting at age 73 or 75, depending on the year you were born.

Overview of Roth IRAs

Roth IRAs are funded with after-tax dollars. While contributions aren't tax-deductible, you'll get tax-exempt growth on your investments and tax-free withdrawals in retirement.

- Eligibility: Anyone with earned income can contribute to an account, although Roth IRA income limits apply. Your ability to contribute may be reduced or phased out at higher income levels.

- Contribution limits: Roth IRAs are subject to annual contribution limits, which are often adjusted annual to account for inflation. Individuals age 50 and older are eligible for higher contribution limits.

- Early withdrawals: You can withdraw your original contributions at any time without taxes or penalties. However, withdrawing earnings before age 59 1/2 may result in income taxes and a 10% penalty unless an exception applies.

- Withdrawals in retirement: Qualified withdrawals in retirement are tax-free if you're 59 1/2 or older and have satisfied the 5-year holding requirement. Unlike traditional IRAs, Roth IRAs aren't subject to RMDs during the original account owner's lifetime.

See our guide to annual IRS updates for retirement plans for up-to-date contribution limits, income phase-outs and withdrawal rules for both Roth and traditional IRAs.

How to choose between a Roth and traditional IRA

For many, the choice between a Roth IRA and traditional IRA comes down to a few key factors, including eligibility, your preferred tax break, withdrawal rules and the potential implications for your beneficiaries.

1Determine your eligibility

With traditional IRAs, anyone earning an income can contribute up to the annual limit. However, if you or your spouse has access to a retirement plan at work—even if you don't contribute—your ability to deduct contributions may be limited.

Your eligibility for a Roth IRA depends on your modified adjusted gross income. Your ability to contribute begins to phase out at certain income levels and is eliminated at higher levels. While the exact limits may change annually, individuals must earn less than the top threshold established by the IRS. These thresholds are adjusted for inflation and updated by the IRS each year.

These traditional and Roth IRA income limits don't apply if you're converting funds from a traditional IRA to a Roth IRA or rolling over a 401(k) to an IRA.

2Choose your tax break

While it's not easy to predict, consider what you think your tax rate may be during retirement. If you expect it to be lower—which is the case for many individuals—a traditional IRA may be the best option. You'll get an upfront tax break now when your tax rate is higher. Once you enter retirement and begin taking withdrawals, you'll pay taxes at a lower rate. This is a common situation for many retirees, who pay the highest taxes during their peak earning years.

If you anticipate being in a higher tax bracket in retirement, a Roth IRA may be a better fit. In this case, you'd pay taxes on your contributions now at a lower rate and benefit from tax-free withdrawals later.

3Evaluate withdrawal rules and penalties

With a traditional IRA, you'll owe income tax on withdrawals, plus a 10% penalty on any funds you take out before age 59 1/2. Certain exceptions—such as a first-time home purchase or qualified higher education expenses—may waive the penalty, although income taxes may still apply.

Following changes introduced by the SECURE Act 2.0, you must begin taking annual RMDs from a traditional IRA account by age 73—or age 75 if you were born in 1960 or later.

With a Roth IRA, withdrawals are more flexible. You can withdraw your original contributions—but not your investment earnings—at any time, for any reason, without taxes or penalties. Once you're over age 59 1/2 and have held your account for at least 5 years, you can withdraw your earnings tax- and penalty-free. Roth IRAs aren't subject to RMDs during the original account owner's lifetime.

4Consider your beneficiaries

If you plan to pass any portion of your retirement savings to beneficiaries, you may also want to consider inherited IRA rules before making a selection.

For example, an adult child who inherits a traditional IRA may be required to pay income taxes on any money they withdraw, and they must empty the account within 10 years. Once you've started taking RMDs, they may also be required to continue these distributions. Plus, if your heirs aren't classified as eligible designated beneficiaries, they may face unavoidable tax liabilities.

With a Roth IRA, beneficiaries generally aren't taxed on qualified withdrawals as long as the account has been active for at least 5 years. They also won't be required to take RMDs, although they may still be required to empty the account within 10 years. As a result, a Roth IRA may carry less of a tax burden for some beneficiaries.

Common questions about IRAs

As you decide between a Roth and traditional IRA, you may still have questions about your options. Here are answers to some frequently asked questions about IRAs.

Can you have both a Roth IRA and traditional IRA?

Yes. You can contribute to a Roth IRA and traditional IRA during the same year, as long as your total contributions for both don't exceed annual limits.

What investments work best in a Roth IRA versus traditional IRA?

With both accounts, you'll have the ability to choose IRA investments like stocks, bonds and mutual funds. A Roth IRA may be a tax haven for growth-oriented investments, but it's a good idea to talk to a financial advisor before making any investment decisions.

Can you convert a traditional IRA to a Roth IRA?

Yes. Roth conversions are a popular strategy, particularly for those who are retired but haven't started taking RMDs. Be aware that you'll owe income taxes on any funds you convert, so it's wise to consult a qualified tax advisor and financial planner before moving funds.

What is a backdoor Roth IRA?

A backdoor Roth IRA uses the same conversion process to help higher-income individuals fund a Roth IRA. It typically involves making a nondeductible contribution to a traditional IRA and then converting these funds to a Roth IRA. While the contribution itself is made with after-tax dollars, you may still owe taxes on any pretax funds or earnings at the time of conversion, so it's important to understand how this strategy fits into your overall tax situation.

The bottom line

Both traditional and Roth IRAs can be useful retirement savings tools—whether you're using them as part of a self-employed retirement plan, to supplement an employer-sponsored plan or simply to reap the tax benefits.

When choosing between a Roth IRA versus traditional IRA, determine when you want to receive tax benefits. If you're hoping to reduce your tax burden today, a traditional IRA may be the right option. If you'd prefer not to worry about taxes later in life, you might benefit from setting up a Roth IRA.

No matter which path you choose, learning more about how IRAs work and speaking with a financial advisor or tax professional before making any decisions can help you make the most of your account.

Ready to get started?

Understand your options so you can make the most of retirement planning.