How to build a corporate payment strategy that scales

Early in a company's growth, convenience often drives payment decisions. As the business scales, however, these same choices can create fragmented workflows, delay cash flow and add to risk exposure. What once functioned as a background process becomes a constraint that demands closer attention.

A thoughtful corporate payment strategy creates alignment across cash flow, customer experience and risk management. Rather than reacting to issues as they arise, your organization can use payments to support growth.

Key takeaways

- As your business grows, a deliberate payment strategy becomes essential to reduce inefficiencies.

- Effective strategies balance efficiency, customer experience and control across payment methods.

- Phased modernization of payment systems reduces risk while supporting long-term growth.

When to think about a corporate payment strategy

Early payment decisions are often made to support speed and simplicity, not long-term scale. As transaction volume increases, these can unfortunately lead to manual workarounds, delayed receivables and limited visibility into cash flow.

"Most businesses don't start out with a formal payment strategy," says Matt Ribbens, head of Treasury Product Management at First Citizens. "Early on, you're focused on growth, so you accept payments in whatever way is easiest or most convenient. It's only as you scale and add controls that delays or inefficiencies begin to surface," he adds. "That's when payments become something you need to step back and look at more intentionally."

As organizations scale, a common set of warning signs often emerges:

- Heavy reliance on manual or paper-based processes

- Customer dissatisfaction with payment options

- Rising costs or delays tied to payment handling

- Limited visibility into cash inflows and outflows

At this point, payments move from an operational detail to a strategic consideration. The goal is no longer to keep transactions moving but to design a system that supports scale, visibility and control through deliberate payment method optimization.

How do you build a corporate payment strategy?

You should build a modern payment strategy in stages, rather than through sweeping change. The most effective approaches focus on a few priorities that can improve efficiency and visibility over time.

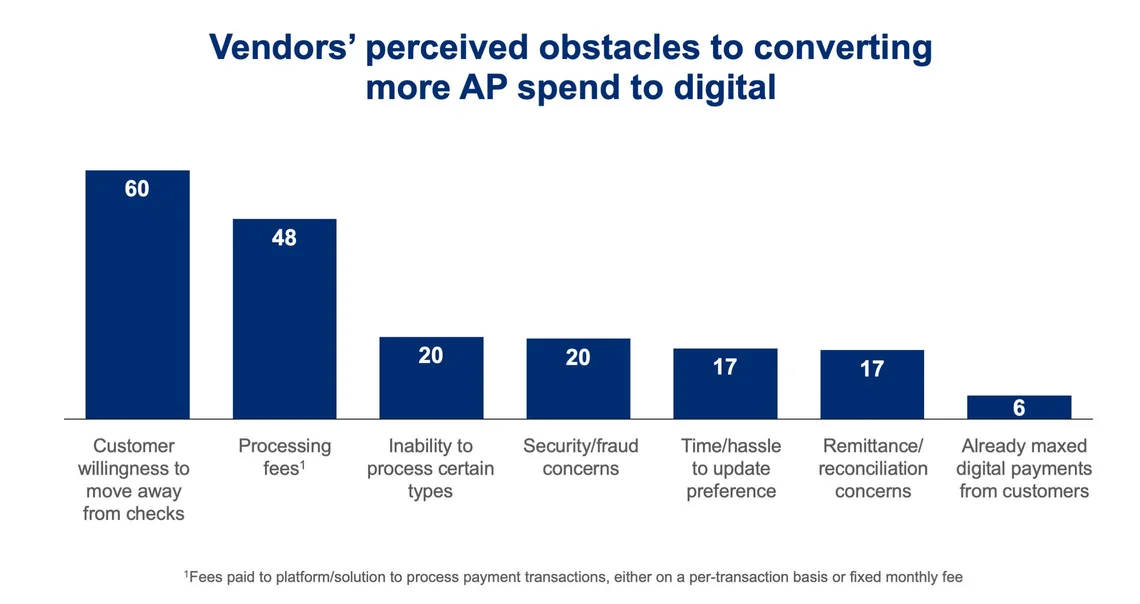

"One of the biggest reasons B2B payments haven't moved faster to digital is that suppliers still control how they want to be paid," says Amit Gandhi, Associate Partner at McKinsey & Company. "Even when buyers are motivated to move away from checks, it doesn't always translate into adoption. Legacy workflows, comfort with checks and fragmented systems often keep those behaviors in place."

The good news is there are ways you can move from reactive payment decisions to a more deliberate strategy. Consider these options.

- Assess volume and relationships. It's important to understand how money actually moves today. Begin by reviewing inbound and outbound payment volumes and identifying key customers and suppliers. This payment method optimization analysis looks for concentration risks, bottlenecks and areas with heavy manual work. Separating receivables from payables often reveals distinct challenges and opportunities on each side of the ledger.

- Strengthen fraud prevention. As payment volumes grow, the need for consistency and visibility increases. Electronic payment methods can reduce risk—but only when paired with the right safeguards. Fraud prevention tools such as ACH filters, positive pay and transaction monitoring can help you reduce exposure while maintaining efficiency. Framing fraud prevention as a resilience issue rather than a compliance task may shift how teams think, and this can elevate its importance across the organization.

- Use card payments strategically. Card payments aren't appropriate for every transaction. However, in the right use cases they can improve speed, customer experience and working capital flexibility. Commercial card programs also help extend payment terms, simplify reconciliation and improve cash flow timing. The goal isn't universal acceptance but rather intentional use aligned with business needs.

Payment modernization rarely happens all at once. Organizations that make steady progress align strategy with operational realities. They prioritize improvements that deliver visibility, efficiency and control without disrupting critical relationships.

How does card acceptance influence revenue and spending?

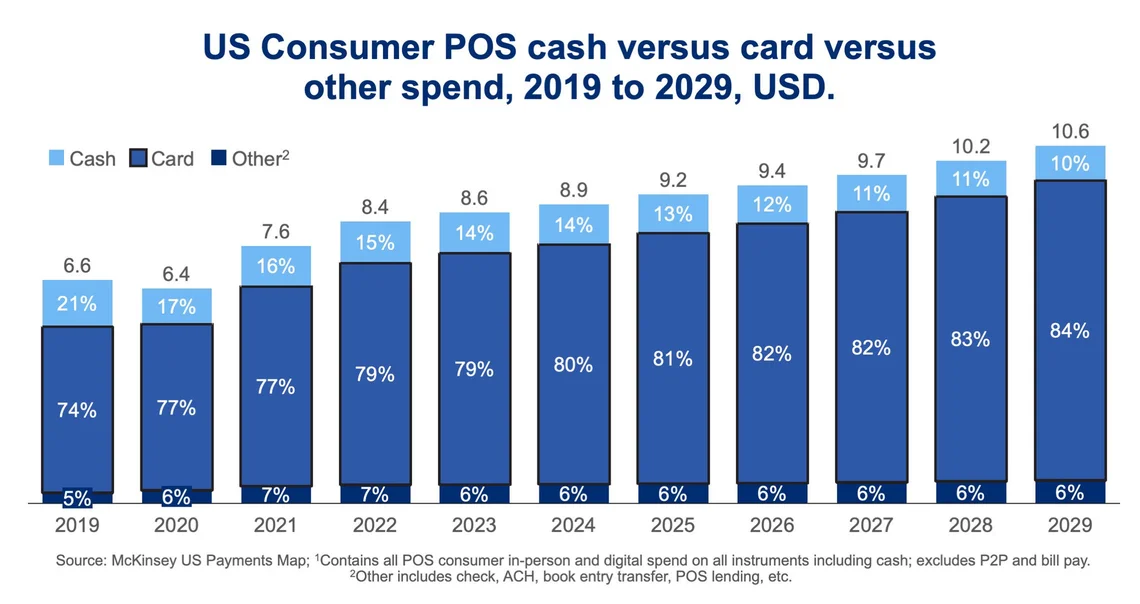

Payment friction can directly affect how and when customers choose to spend. Consumer data consistently shows that card payments remain the preferred method at the point of sale, with cards continuing to gain precedence over cash.

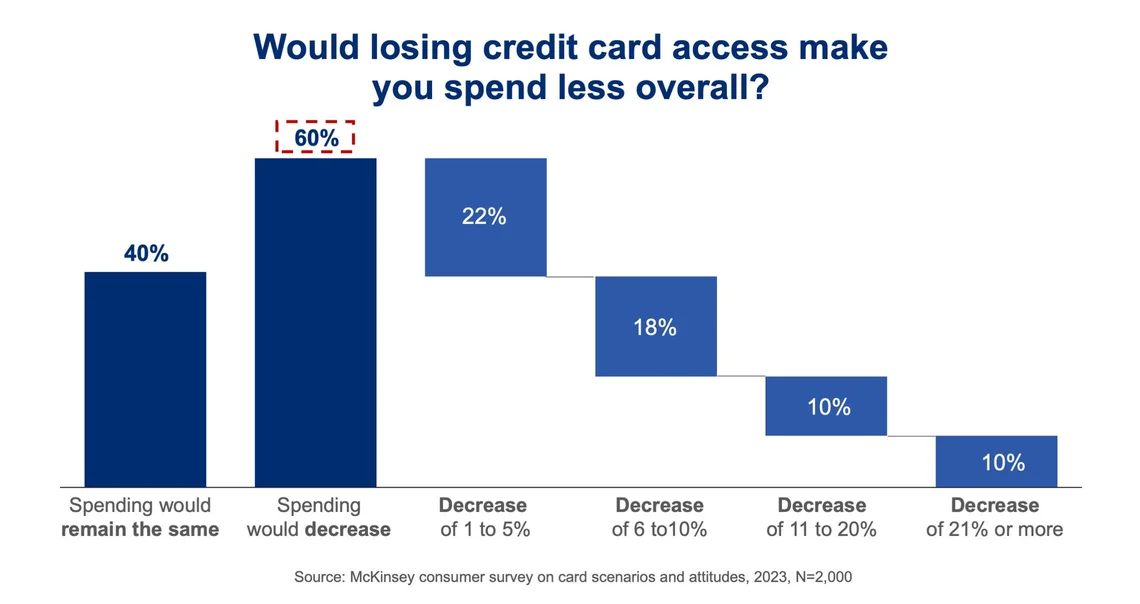

More importantly, access to credit influences purchasing behavior. Research indicates that many consumers would reduce overall spending if they lost access to credit cards.

But while consumer preference is a major driver, cost considerations remain a big part of the equation—particularly in low-margin environments. Processing fees are real, but pricing models have evolved to include surcharges, convenience fees and dual pricing. These options give your business more flexibility than in the past, allowing you to balance customer experience with profitability.

Fraud perception often complicates this conversation. "When you look at the data, fraud attempts on checks are higher than what we see across ACH real-time payments and virtual cards combined," Gandhi says. "Yet many businesses still perceive checks as safer. That perception gap continues to slow adoption of more secure digital payment methods."

Opportunities for card acceptance remain strong in underpenetrated industries and nontraditional use cases—including professional services, utilities, rent and certain B2B payment scenarios where buyers seek flexible payment terms. In these environments, align payment options with customer expectations to reduce friction and support growth.

How is the payments landscape changing?

Payment behavior continues to shift, although adoption moves at different speeds for consumers and businesses.

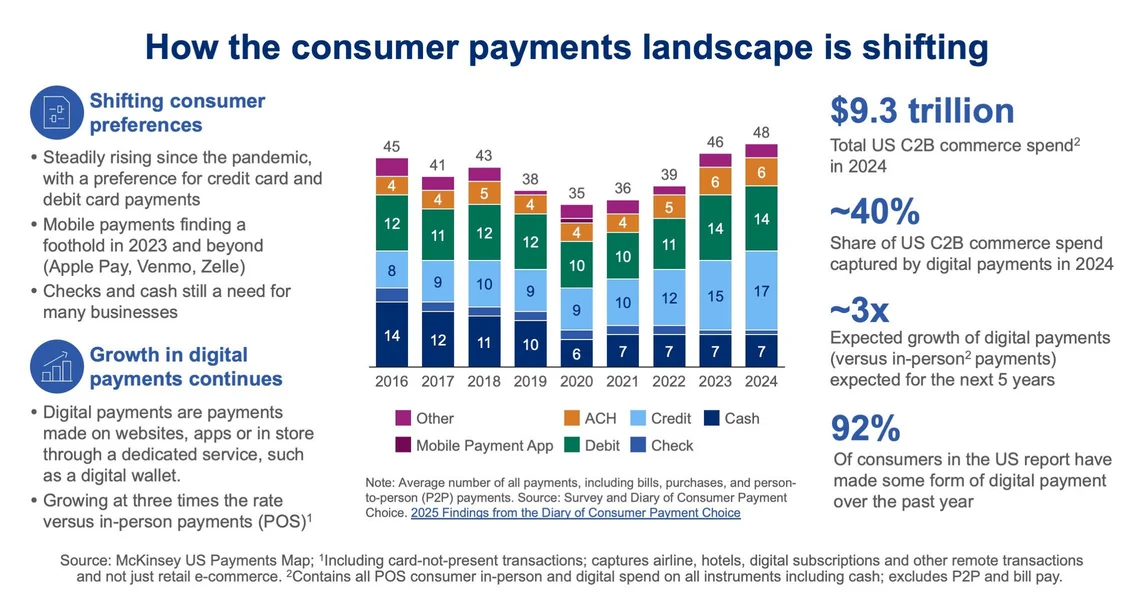

On the consumer side, card-based and digital payments continue to grow in market share —driven by convenience, speed and familiarity. Mobile wallets have expanded the payment experience, enabling faster and more seamless transactions while still relying primarily on existing card infrastructure. Cash and checks remain in use for certain situations, but their overall share continues to decline.

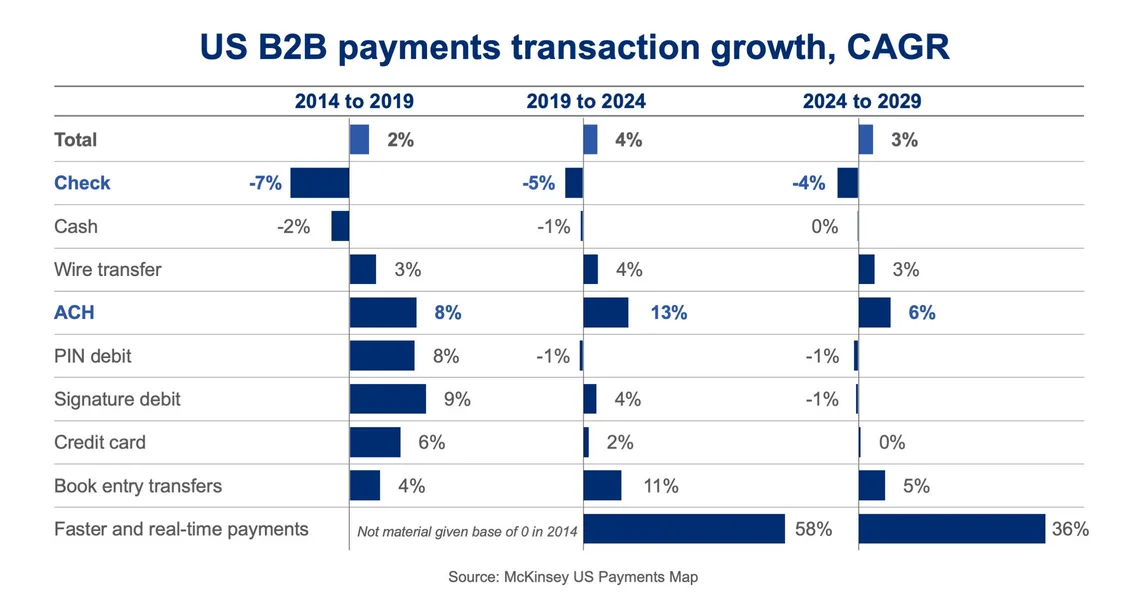

Business payments follow a similar trajectory but at a different pace. Checks are gradually giving way to electronic methods, with ACH emerging as the primary beneficiary due to its scalability, low cost and reconciliation advantages. Real-time payments are growing, but adoption remains uneven. In many cases, access and pricing remain barriers, while many transactions simply don't require immediate settlement.

"As consumers, we've all gotten used to frictionless payment experiences in our everyday lives," says Jason Mills, head of Merchant Services at First Citizens. "That same expectation carries over into business interactions, and companies that adapt their payment strategies to meet this reality tend to see better engagement and stronger results."

Several emerging payment types are also attracting attention, particularly stablecoins. However, most stablecoin activity today remains concentrated outside of everyday payments—with use cases still largely limited to trading and on- and off-ramping. For most domestic transactions, established rails such as ACH and cards continue to meet a majority of business needs. Cross-border payments represent the most practical, near-term use case as the technology continues to mature.

What does a smarter payment strategy look like?

There's no single payment mix that works for every organization, and effective payment strategies should evolve alongside the business.

In practice, this often means revisiting long-standing assumptions about how payments should work day to day. Regularly reassess payment methods, involve stakeholders beyond finance, and evaluate decisions through both operational and customer lenses to stay aligned as complexity grows.

Partnering with treasury management experts who understand that both banking and B2B payments can also play a role. External perspective can help you identify opportunities for improvement, navigate trade-offs and design strategies that are realistic, scalable and aligned with business goals.

The bottom line

As your business grows, payment processes that once worked by default can begin to break down. They slow cash flow, reduce visibility and add operational friction.

A deliberate corporate payment strategy helps you address these pressures in a measured way—balancing efficiency, customer experience and control as needs evolve. Ultimately, when payments are treated as infrastructure instead of an afterthought, they're better positioned to support growth rather than slow it. And when B2B payments are treated as part of a broader strategy, you're better positioned to grow with control and confidence.

To explore how a more intentional approach to payments can support your next stage of growth, get more insights and resources from First Citizens Treasury Management.