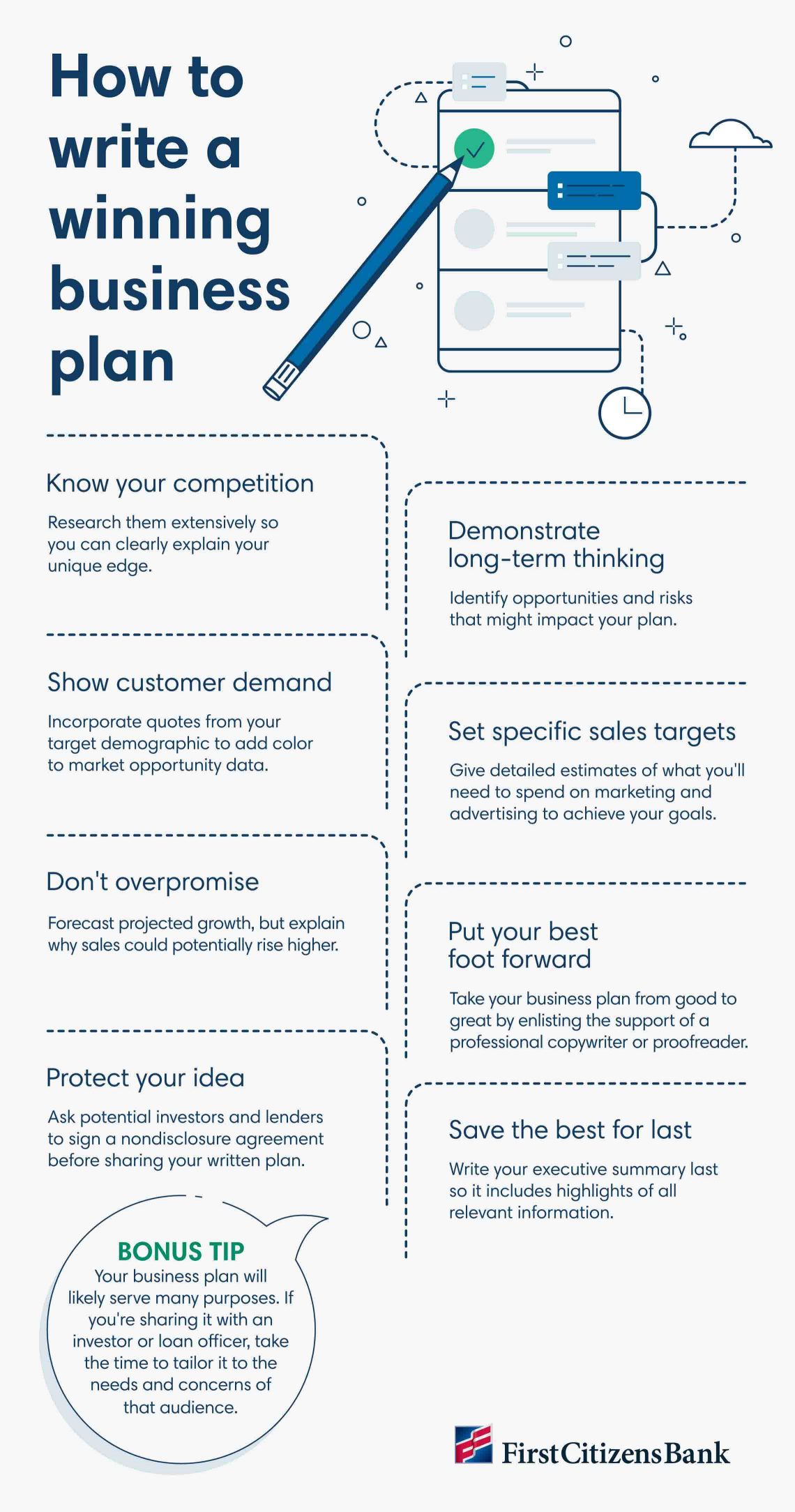

How to Create a Business Plan

Whether you're getting ready to launch your small business or preparing to seek outside funding, a good business plan is essential. It can help you outline crucial elements of your strategy, establish key business goals, identify potential barriers and evaluate your achievements over time.

When done right, your business plan can continue to serve as a roadmap for your business over the next several years. Think of it as a living document—one that continues to be updated regularly as your business grows and evolves.

The purpose of a business plan

Unless your small business is entirely self-funded, you'll likely need to rely on some form of outside funding. If you're applying for a bank loan or seeking the support of a venture capitalist, you may be asked to share a copy of your business plan.

However, its purpose extends much further. Here are a few additional benefits of a business plan for a small business.

- It expresses your vision and strategy to potential stakeholders and employees.

- It provides you with critical insight into your target customers and competitors.

- It guides wise decision-making to maximize profitability.

While knowing how to create a business plan may not come naturally, taking the time to create a thoughtful, strategic business plan is often worth the investment.

Elements of a business plan

Whether you're hoping to land on the Fortune 500 list or simply start a side hustle, a basic business plan for a small business should include the following components.

Executive summary

Create a concise overview of your business's mission, and explain why you believe it will succeed. Key elements include:

- An overview of your offerings and the problem you're solving

- A brief competitive analysis and explanation of what sets you apart

- Your typical customer profile and a target market overview

- A high-level overview of your goals

- Financial projections and funding requirements

Company description

One of the main purposes of a business plan is to clearly communicate essential information about your company. A good place to start is by sharing a mission statement. You may also want to include descriptions of your:

- Company structure and leadership team

- Philosophy and core values

- Short- and long-term goals

- Key performance indicators

- Legal structure or business type

Learn more about the various types of business ownership to determine the right legal structure for your small business.

Products and services

Describe the range of products or services your business will offer, including key features and benefits. As you draft this portion, be sure to:

- Explain how you'll produce your products and identify who will provide key services

- Discuss your pricing strategy and the costs associated with your products or services

- Highlight patents, copyrights, licensing agreements or exclusive partnerships with suppliers

Market analysis

Demonstrate your understanding of your industry, key competitors and your target market. Show why your product or service stands out and deserves a spot in the existing marketplace. Be sure to include:

- Industry trends and themes

- Market size and demand

- Risks and opportunities

- Projected revenues

- Market research

The US Small Business Administration is a useful resource for data and insights, as are industry associations and large consulting firms.

Marketing and sales

This is your opportunity to describe your approach for reaching your desired audience through marketing and advertising. Be sure to:

- Provide specifics on any tactics you'll implement, such as advertising, social media marketing or potential partnerships

- Clearly describe your sales process, including any initiatives to increase sales

- Incorporate expansion strategies and provide marketing budget estimates

Funding and financing

Anyone who's investing money or time into your business—including lenders, mentors and leadership hires—may look to this section of your plan for evidence that your business will be profitable.

If you're just starting out and don't have a financial history yet, this section may take a bit more work. Be sure to:

- Outline your plan to fund the first 3 years of your operations, including projections for medium-term growth

- Include recent financials

- Make a list of all outstanding debts and a 5-year forecast of income and expenses

If you're seeking outside funding, this section should also clearly address how much capital you'll need and how it'll be used.

Planning for business success

A solid business plan include goals that are specific, measurable, attainable, relevant and time-bound, or SMART. Just make sure your goals align with your company's overall mission and long-term vision because they'll be key drivers of your success.

In addition to outlining the purpose of each goal, your business plan should detail any strategies or tools you'll implement, such as a customer loyalty program or themed discount days. To effectively measure and track your progress, break down larger goals into smaller, manageable tasks with defined timelines.

The type of business plan you create could be traditional and comprehensive or nontraditional and lean—or it could fall somewhere in between. Comprehensive business plans typically dive deeper into specific data and analysis, while lean business plans focus on summarizing only the most essential points of your business.

The bottom line

While creating a business plan can be a time-consuming endeavor, a thorough, well-written plan is often worth far more than the effort and research involved in putting it together. In fact, it may be the determining factor between an unrealized pipe dream and a well-executed company that's thriving thanks to investor and lender buy-in.

Questions about SBA term loans?

If you're starting or expanding a business, an SBA term loan could be an option to help secure the capital you need.