Strategies to Consider as Student Loan Payments Resume

If you've been keeping your fingers crossed that some or all of your student loans would be forgiven, it's time to reassess your strategy.

With the US Supreme Court striking down President Joe Biden's plan to eliminate up to $20,000 of student debt for most individuals, now's the time to determine your next steps if you still owe.

Switching gears on repayment

The Biden Administration responded with a plan that would still discharge about $39 billion in student loan debt for more than 804,000 borrowers through tweaks in the way rules are interpreted on income-driven payment plans.

However, as a result of the Supreme Court's decision, debt relief will be limited to far fewer borrowers. For most, interest accumulation on student loans—which had been paused since the COVID-19 pandemic first hit in 2020—will resume on September 1, 2023, with payments becoming due starting the following month.

The good news is that you have some time to determine your strategy, and new options are in place that could help reduce monthly debt payments for many borrowers. And there's still a bit of time to revamp your monthly spending budget to prepare for the impact.

"We're no longer in wait-and-see mode on student debt," says Craig Shively, wealth paraplanner at First Citizens Investor Services. "Given that there are a few months until student loan payments resume, now's a great time for most borrowers to revisit their budgets and consider reducing their discretionary expenses as they transition back into loan repayment mode."

Here are some steps you can take to make sure you're ready come September.

Step 1: Understand what you owe

Because student loans have been in forbearance for more than 3 years, your first step is to make sure you know what and to whom you owe. Some of your student loans may have changed hands, so you'll want to go online and check that any automatic payments you had set up are going to the correct institutions.

If you have automatic payments, double-check which account they're drawing from. If you've changed banks, started a new checking or savings account or made other financial changes during the past few years, you may need to update your information with your lender.

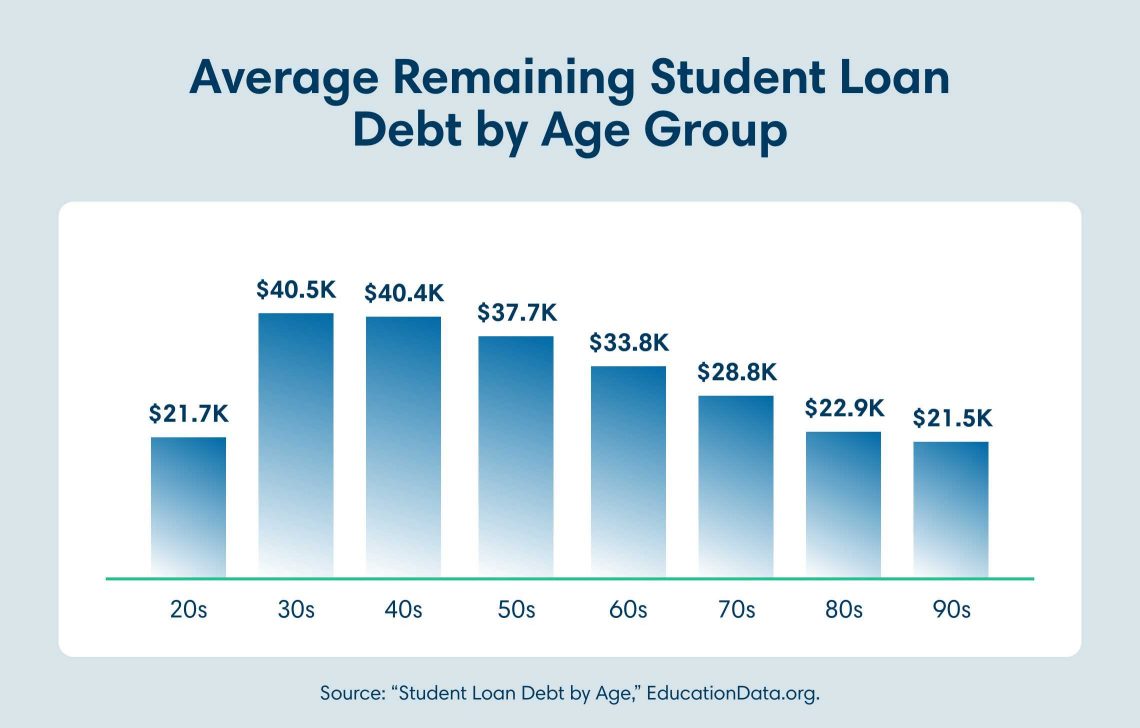

The following are the average remaining individual student loan debt amounts by age group, according to the Education Data Initiative:

- 20s: $21,700

- 30s: $40,500

- 40s: $40,400

- 50s: $37,700

- 60s: $33,800

- 70s: $28,800

- 80s: $22,900

- 90s: $21,500

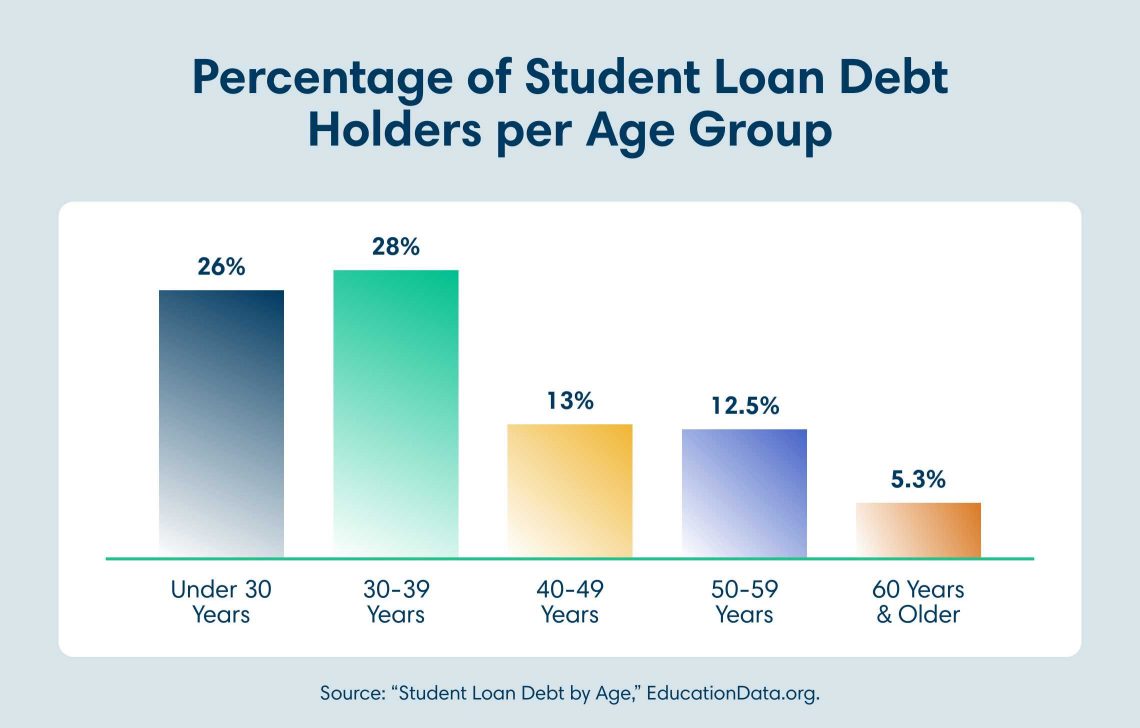

Overall, the percentage of student loan debt holders per age group skews toward younger debtors:

- 26% is held by people younger than 30

- 28% is held by people in their 30s

- 13% is held by people in their 40s

- 12.5% is held by people in their 50s

- 5.3% is held people 60 and older

Step 2: Check your interest rates

While you're checking in with your lenders, it's a good idea to review the interest rate on each of your student loans. Like other types of loans, student loans can have either fixed or variable interest rates.

If you have variable-rate student loans, you may notice that interest rate hikes over the past year have made your interest rate higher than you remember it. As a result, when payments resume you'll be paying more in interest than you were before, and it may take you longer to pay off your loan—and cost you more in the long run.

Even with rates higher than they were in 2020 when forbearance began, refinancing your student loans could still be an option. Refinancing your student loans is essentially moving your debt from one lender to another one.

If you qualify to refinance based on your credit history, employment status, income, cash flow and the amount on your student loan debt, there's no limit to how many times you can refinance. However, refinancing may involve fees, could impact your credit score and can make repayment take longer.

Step 3: Consider life changes

Did you get married since the pandemic began? Has your job status changed, or did you get a significant pay boost? The changes in your life may impact how you approach paying your student loans again.

Married couples may be able to consolidate their separate student loans through a private lender, which could potentially give you a lower interest rate or simplified repayment terms. Similarly, if you were on an income-based repayment plan prior to forbearance, changes in your work status and pay may play a role.

If you're considering consolidating loans and moving from federal student loans to a private loan, it's important to remember that you'll lose access to any federal repayment or loan-forgiveness programs. Talk to your financial professional so you're aware of the benefits and challenges of all options.

Step 4: Learn about repayment options

While the broad plan for student loan forgiveness was struck down, there are still many new federal programs or changes to existing programs that may impact how you approach repaying your student loans. Reviewing these to see which may work best for you is an important step.

Saving on a Valuable Education

Saving on a Valuable Education, or SAVE, is the US Department of Education's new income-driven repayment program that replaces the previous Revised Pay-As-You-Earn, or REPAYE, program. Parts of it won't go into effect until July 2024, but two key provisions will be available starting this summer to help with the transition back to student loan payments.

- Income threshold: The income threshold changes for how your disposable income is determined. Generally speaking, the lower your disposable income, the lower your required monthly payment. Previously, income up to 150% of the federal poverty guidelines was protected. This increases to 225% of federal poverty guidelines in the new program. A single borrower who earns less than $32,805 per year won't have to pay on their loans. For a family of four, the income figure is $67,500.

- Monthly interest: Borrowers making their regular payments through SAVE won't be charged monthly interest beyond what's covered by their monthly payment.

When the additional rules go into effect in 2024, payments on undergraduate loans will be cut in half, from 10% of the disposable income calculation to 5% of this amount. Loan forgiveness for some loans, depending on the original amount borrowed and the number of payments made, will also be available.

Pause on default

After the Supreme Court decision, President Biden announced a 1-year grace period of sorts for borrowers who may struggle to resume loan payments. During this time, interest will continue to accrue, but borrowers won't go into default until a year's worth of missed payments has passed.

However, because interest will still accrue the smart choice is to begin making payments as quickly as you can.

The bottom line

If you saved during the years of forbearance and are in a better financial position than you were in 2020, you could consider a lump-sum payment in advance of payments coming due. This could help you pay off your loans sooner and save on interest that would accrue over time, meaning you'll pay less in total.

However, as when choosing any debt-payment strategy, it's important to consider the interest rate of your student loans compared to any other existing debts, such as credit cards.